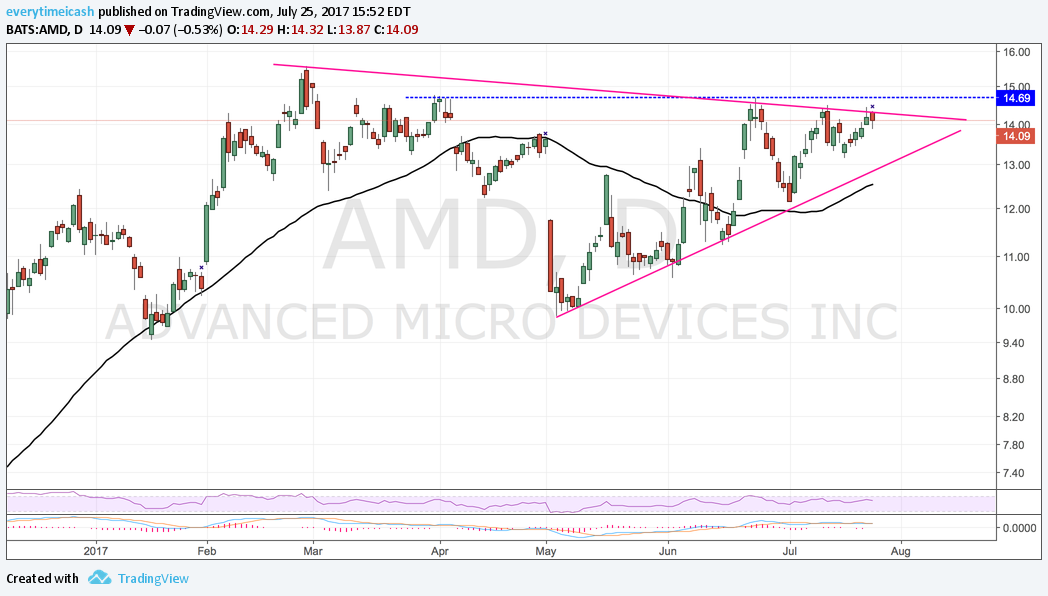

AMD (AMD) will report Q2 results after the bell and host a call at 5pm.

The Street is looking for Q2 adj. EPS of $0.00 versus ($0.05) last year with rev up 12.7% Y/Y to $1.16 bln versus $1.12-1.18 bln guidance (+14-20% Q/Q).

AMD has guided for low double-digit revenue growth, gross margin expansion and non-GAAP net income -- FY17 non-GAAP EPS consensus $0.07 with revenue +12.8% to $4.82 bln.

AMD is the number two player in both CPUs and GPUs behind NVDA. The stock's comeback has mostly come on the heels importance of GPUs. Cryptocurrency mining has also created demand for GPUs.

AMD stock is not cheap at 3x FY17 sales or 45x EV/EBTDA... 2.6x FY18 sales or 26x EV/EBITDA

RESULTS

Advanced Micro beats by $0.02, beats on revs; guides Q3 revs above consensus; raises FY17 sales growth

- Reports Q2 (Jun) earnings of $0.02 per share, $0.02 better than the Capital IQ Consensus of ($0.00);

- Revenues rose 19.0% year/year to $1.22 bln vs the $1.16 bln Capital IQ Consensus, driven by higher revenue in the Computing and Graphics segment.

- Revenue up 24% sequentially, driven by increased sales in both business segments.

- Gross margin was 33 %, up 2 percentage points year-over-year due to a richer product mix and a higher percentage of revenue from the Computing and Graphics segment, driven by the first full quarter of Ryzen processor sales.

- Computing and Graphics segment revenue was $659 million, up 51 percent year-over-year, driven by demand for graphics and Ryzen desktop processors.

- Operating income $7 million, compared to an operating loss of $81 million in Q2 2016. The year-over-year improvement was driven primarily by higher revenue and improved product mix.

- GPU ASP increased year-over-year. Enterprise, Embedded and Semi-Custom segment revenue was $563 million, down 5 percent year-over-year primarily due to lower semi-custom SoC sales. In the quarter, AMD reached an important milestone by recognizing initial revenue from EPYC datacenter processor shipments.

Co issues upside guidance for Q3, sees Q3 revs of +20-26% Q/Q to ~$1.47-1.54 bln vs. $1.39 bln Capital IQ Consensus Estimate; adj. gross margin ~34%.