“Do not anticipate and move without market confirmation—being a little late in your trade is your insurance that you are right or wrong.”

There are no better times for the market’s snake oil salesmen than a raging bull market. Whether it’s “buy the dip” or “buy right sit tight” or any other God forsaken cliche line they repeat, everyone is a “genius” when the markets rage on. From Bitcoin to tulips, pundits will continue to tell you what to do while collecting your money. However, all good scams must come to an end. That end is typically spelled out when the “music stops” and the old idioms no longer work. That said, this is one of those times. A time that “separates the men from the boys” or whatever other garbage saying you want to insert.

Catalyst

For an exogenous event to transpire, a catalyst is often needed to set the move into action. Just like in 2008, 1999, or any other moment in time, that catalyst is often unbeknownst to the masses or simply ignored. In our case, it appears that our exogenous event began a couple of weeks ago when Fed Chair Powell tilted the Fed’s hand to a more hawkish tone.

The Fed

It all started at the Fed’s press conference following their rate decision. It was further exacerbated when Powell told PBS News House that the “next set of problems wouldn’t look a lot like the last set of problems we had. He went on to state that it “would be something else, a cyber-attack, some type of global event. Or maybe it will surprise us and look exactly like the last one.”

These comments were telling. If there is one thing the markets do not like it’s uncertainty. Those comments came off as though the Fed doesn't really have a tell on what the next scare will be. That alone is troublesome, it was compounded further with the following quote:

“The really extraordinarily accommodative low interest rates that we needed when the economy was quite weak, we don’t need those anymore, they’re not appropriate anymore. We need interest rates to be very gradually moving back toward normal.”

As it stands, the the Fed’s target Fed Funds Rate is at a range of 2-2.25%. This, to Powell, is a “long way from neutral.” With that, and with his comments, no one knows exactly where “neutral” is. The comment of “we’re a long way from it” suggests that the Fed may raise past the current neutral rate. That would send short-term rates well past 3% and dauntingly to a potential 4% handle.

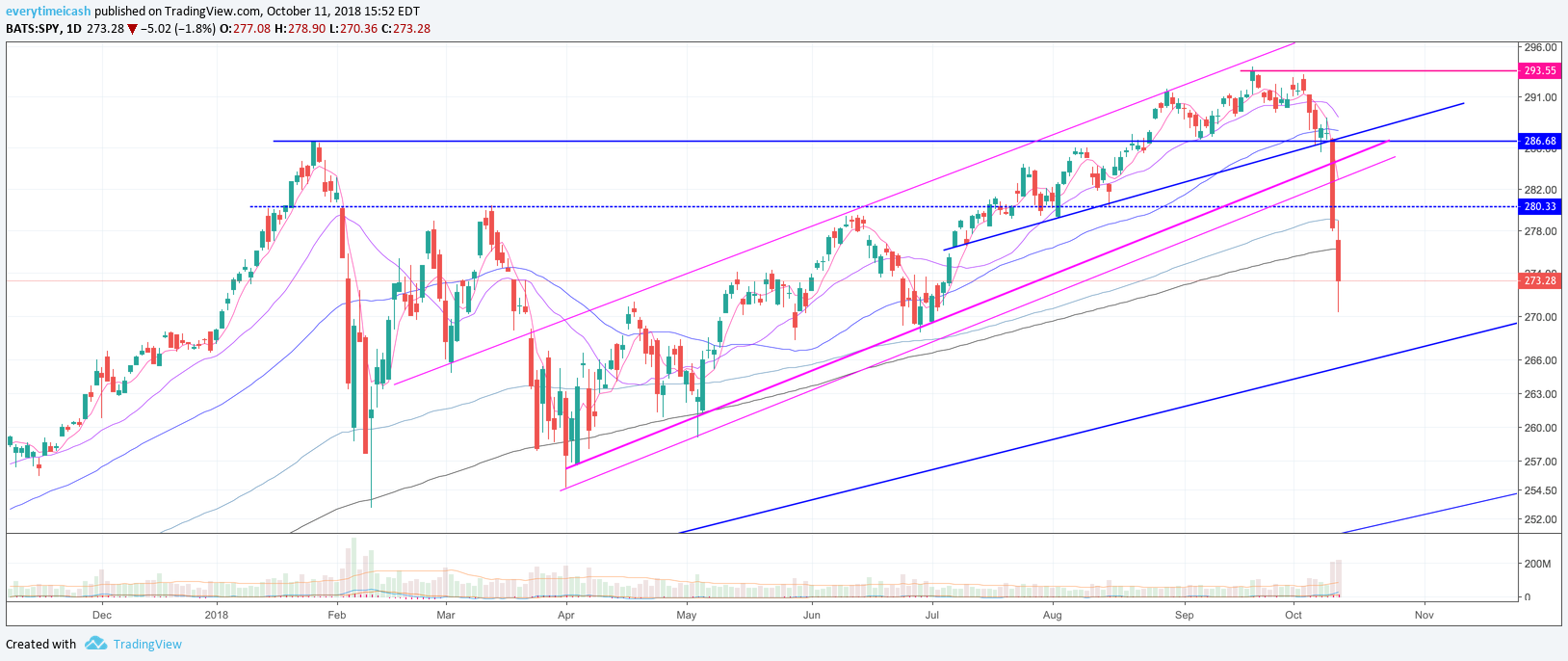

Beyond that, Powell did not hesitate to leave investors in the dark. Simply put, Powell hinted that further acceleration may be in order but did not accommodate that easing would take effect should it be necessary. This was just the first domino. As we later saw (pictured below), this cascaded a series of events that spooked financial markets across the board.

Rates

Not long after the Powell comments, the markets started to take notice. That notice came in the form of the US treasury market. Shortly after the comments, the 10-year yield popped north of 3.25% for the first time in nearly a decade. Stocks in turn fell as investors started to feel the heat. This downdraft hit as investors started to truly evaluate whether the risk premium for all this “free money” was sustainable. Rates appear to have given investors the go ahead as they appear to have bottomed and are basing for further upside.

The interesting part is we’ve seen this narrative before. We’ve seen the rates saga come and go, the yields increase, the cheap money being taken away, and it never seemed to have an impact on the punch drunk bulls. So what changed?

Tariffs

One of the key points to take in is that the Fed is very keen to inflation and inflation concerns. The real concern you need to know about here is that as of late last week and early this week a real fundamental fear of (artificial man made) inflation in the form of tariffs started to creep into the market. Investors were spooked as the reality that inflation could creep into the market while the fed stands pat on their normalization path. Typically, to offset inflation, the Fed will increase interest rates at a gradual pace. IF there is an artificial inflationary event/situation this could cause the Fed to increase rates at a much faster pace to curb inflation. Many believe it is this fear that started to accelerate market worries this week as Fed Chair Powell did not hint that the Fed would consider lowering rates should the inflationary concerns be artificial.

The Turn

Though much of this seems “obvious” today, it was not so just a few days ago. I’ve spent the better part of the past week watching every Tom, Dick, and Harry try to buy the dip and get washed. I alerted both the internet and people who follow me closely to stay away from buying dips for the foreseeable future and we have been rewarded in kind for heeding that warning.

You see, though I am primarily a momentum and technicals trader, I have been around long enough to see market corrective behavior. I survived/thrived during the Financial Crisis and took with that some lessons. The main fundamental take away that I can share is the charts are just PART of the equation. In a raging bull market everything works technically. You buy the dip off of a support level, you watch it rally to oblivion, you get rich. You buy a breakout, you get rich. You HODL, you get rich. When that tide swells however, you have got to pay attention.

When price action is poor following a catalyst, take notice.

Where To?

We’ve now seen a correction of some kind in the markets and have seen some of our leadership get obliterated. So it’s pretty easy to wax poetic about how you should have done this, or should have done that. The key now is to figure out where we go next.

I am of the belief that the market is, for lack of a better term, fucked. On an equal weight basis, the market did not create a new all time high after plummeting from it’s original high back in February. We did however create very critical double tops across the board in many sectors. Eight of eleven sectors never reclaimed their peaks and have been in perpetual spiral mode for what feels like an eternity. Tech leadership has waned and a paradigm shift into “safer” asset classes does not bode well for them.

With all of that said, we did happen to be in a seasonally dead period as share buybacks were dried up prior to earnings reports. Because of that, the blow we faced came quick and in a hurry. We have ultimately snapped the 200 day moving averages of all major averages.

That said, RSI is really low and regardless of the selling catalysts we are likely due for some form of sideways action or a short rally. Earnings will likely spark a catalyst for such an event as investors step in and scoop up depressed assets with solid reports. Personally, I do not believe that it will be enough in the longer run as I am of the bias that this will just create a perfect opportunity for another selling event to take hold. From my experience, when assets break multi year trends and moving averages after failing to sustain new highs it is not a good sign of things to come.

Catalyst 2.0

In order to forecast where we are and where we are going, we have to consider some possible catalysts for a move. Below I will highlight a few to keep track of.

Fed Decision in December

Everyone and their brother believes the Fed will move again in December. So with that said, should the Fed not move given President Orange’s comments as of late this would spark some real fear that the Fed is not moving solely at the discretion of data.

Jhina (China)

US China trade tensions could potentially escalate as it is my bias that the Chinese have more leverage to stand on given their absence of political necessity. At the end of the day President Orange is still in a popularity contest given how the US political system works. Given that the Chinese do not have political impetus it is my bias that they have more room to stand pat than given credit for.

Secondarily, it is no secret that the Chinese hold a ton of US government debt. $1.2 trillion worth to be exact. There is now a fundamental risk and worry that if the trade war materializes into a more serious event China could reduce its US debt holdings as a weapon against the orange guy and his tariffs. In an event that occurs the Dollar would fall and other countries would likely follow suit and sell their holdings as well. Secondarily, if China reduces their exposure at a time when the US increases their supply of new Treasuries into the market, that would lead to a rout in the bond market.

Speaking of bond markets, China’s bond market is bucking the trend of the global sell offs. Not so ironically, China is is seeing lower yields in its bond markets due to an inflow of foreign investment and more liquidity from their central bank at a time when the US is experiencing the opposite. A combination of idiosyncratic and policy-driven factors has been insulating China’s bond market from upward pressure on global yields. This is in part aided by Beijing shifting to a more growth-supportive measure in July to combat the US tariffs. Put into context, China’s 10-year yield has falling ~30 basis points to 3.65% while the US has been ripping.

Performance Chase

The last catalyst to watch for is momentum selling. In the event that the year goes negative fund managers may accelerate the losses into the new year as they chase performance. This would make for an “outside year” to the downside and does not bode well for equities from a historical standpoint.

If any of those catalysts occur, or if real inflation starts to creep up along with the manufactured inflation in the form of tariffs watch out.

Ask Yourself

If you are paying someone for financial advice and they were unable to prepare you with any of this caution prior to the events that transpired this week, or worse, they were telling you to buy the dips, you should no longer pay that individual. We are no longer in a calm bull market. The “Fed Put” is seemingly off the table and has been for quite some time. This is not a self promotional message or endorsement, this is a PSA. There are a lot of scammers and fools out there that will happily accept your money and worse off drive you into the path of self destruction. Please assess your situation accordingly and react to it.

SHAMLESS PLUG AND POD

For the sake of clarity and for the sake of fun, I will be releasing a podcast soon. If you have any ideas for topics or names please message me using the contact page on my site.

If you'd like to follow my trades in real time click the "Join Now" button at the bottom of the page. For those that will and have asked, use the code GUEST on checkout for a discount on your first month with no commitment thereafter.