Netflix ($NFLX) is set to report Q1 results tonight after the close with consensus at EPS of $0.03 on Revenue of $1.965 bln.

Expectations for NFLX are high once again as we await the Q1 report. NFLX had a strong 2015 as International subscriber growth was able to outpace expectations and lead NFLX to a better than expected performance. But the slow down in Domestic was troubling and investors are watching closely to see if the co was able to maintain its momentum in 2016. Some key items to watch include:

- Q2 Guidance: Q2 numbers will be extra important. NFLX raised its price to $9.99 in May of 2014. It provided a two year grandfather clause for those that were in earlier at the $7.99 level. This quarterly outlook will help provide color on how NFLX sees the change impacting results as well as churn for the higher prices.

- International: Recall on January 6, NFLX announced an aggressive push into additional countries which would triple the amount of countries it served. This gives the co with ample opportunity for subscriber growth but comes with high cost.

- Competition: We saw AMZN launch a new streaming service today which will directly compete with NFLX. GOOG's YouTube Red, HBO Now, and AMZN Prime are all providing pressure on NFLX. So comments from the co will be of interest but the impact on subs is what will be watched the closest.

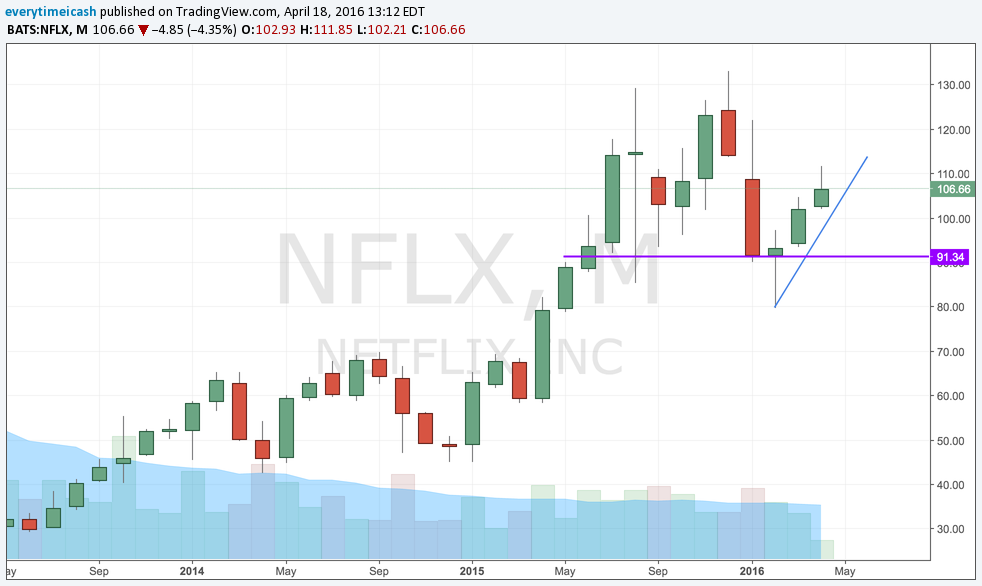

Stock Reaction Last Three Reports:

- Q4- NFLX beat by 8 cents on EPS but missed its top line revenue expectations. This report was released during the early market sell off and would help lead NFLX to break below its 200 sma. It would eventually slide to from the $104 area to $79 on February 89 before finding support.

- Q3- Stock fell approx 10% in reaction as a top and bottom line miss were cause for concern. The stock would hold the $100 psyche support and eventually rally to $134 in the weeks that followed.

- Q2- Stock would rally nearly 20% after the subs number handily outpaced expectations. Revenue was a miss (NFLX has actually missed revenue in the last six reports) but markets did not seem to mind give the sub performance.

Key Metrics/Guidance

Total Streaming

Revenue- Q1 Guidance $1.813 bln, Q4 $1.572 bln

Contribution Margin- Q1 Guidance 16.7%, Q4 16.2%

- Total Membership- Q1 Guidance 80.86 mln, Q4 74.76 mln

- Net Adds- Q1 Guidance 6.1 mln, Q4 5.59 mln

Domestic Streaming

- Revenue- Q1 Guidance $1.16 bln, Q4 $1.106 bln

Contribution Margin- Q1 Guidance 35.9%, Q4 34.3%

- Total Memberships- Q1 Guidance 46.49 mln, Q4 44.74 mln

- New Additions- Q1 Guidance 1.75 mln, Q4 1.56 mln

International Streaming

Revenue- Q1 Guidance $653 mln, Q4 $566 mln

- Contribution Margin- Q1 Guidance -17.5%, Q4 -19.2%

- Net Additions- Q1 Guidance 34.37 mln, Q4 30.02 mln

- Net Additions- Q1 Guidance 4.35 mln, Q4 4.04 mln

- Total (including DVD)

- Net Income- Q1 Guidance $11 mln, Q4 $43 mln

- Free Cash Flow- Q4 ($276) mln

- Content Obligations- Q4 $10.9 bln

Key Comments from Q4 Letter to Shareholders

- Our global availability sets us up for continued growth for many years and we continue to expect material global profits beginning in 2017.

- We are seeing increased adoption of our Ultra-HD plan ($11.99) as more UHD TVs are purchased and as we are a leading source of UHD content for consumers. In Q2 and Q3, we'll be releasing a substantial number of our US members from price grandfathering on the HD plan and they will have the option of continuing at $7.99 but now on the SD plan, or continuing on HD at $9.99 a month. Given these members have been with us at least 2 years, we expect only slightly elevated churn.

- In the last remaining major market, China, we have work and uncertainty ahead. We are building relationships, understanding the market, and seeking the conditions we require to provide our service to entertainment lovers there. Our expectations are modest and long-term. We may be able to get started this year and thus deliver on "whole world by end of 2016" or it may take longer.

- Most of our focus is on the 130 countries we launched on January 6, which are now embracing Netflix as a new entertainment option.

- In 2016, we plan to launch over 600 hours of original programming, up from about 450 hours in 2015. As a reminder, our investment in originals, particularly owned content, requires more cash upfront relative to licensed content, which will continue to dampen free cash flow.

- Given our expected cash needs, we are likely to raise additional debt in late 2016 or early 2017.

We want to see if this incremental bump in UHD subscriptions will have a tangible impact on the top line rev. We don't want to see serious churn now that the price has increased. This could offset any international expansion as individuals don't forsee international subs as revenue drivers in the early adoption period.

TECHS:

Shares of NFLX have been on a steady move higher since hitting its low of $79.95 on February 12. NFLX is sitting on top of two areas of support the 100-sma ($105.53) and the 200-sma ($106.78) . Both levels should function as "support" going into the report and will serve as "resistance" if the issue gets through it.

BIAS: BUY AGAINST THE 200D TODAY. WE WILL LIKELY GET A 20-40% INCREASE IN CALLS PRIOR TO THE REPORT AGAINST THIS LEVEL BELOW.