Since the Feb 11th lows the market has seen its fair share of rotation and short covering. What started in energy and materials has now made its way to biotech. It is apparent that the "Dash for Trash" effect is a painful short squeezing mechanism that seemingly has no end in sight (a la $TSLA).

With that said, this is a good time to find potentially bottoming patterns that are poised to reverse their trends higher. That said, we aren't trying to find dog shit and throw darts at a wall. Bad stocks are usually bad stocks for a reason and it's important for us to distinguish between a bad stock that has been left for dead with no potential hope due to company fundamentals and one that has been left for dead but is fundamentally adequate for a potential turn. It's also important to note that no matter how the fundamentals may look, the stock's chart is often more important as it gives us a visual representation of how a particular stock's psychology looks at the moment. Simply put, if a stock's chart is showing no signs of life we don't want to take a stab at it.

So what exactly are we looking for?

We want to start our shopping for companies with low debt. The lower the debt, the better positioned the company is to use capital to turn their company around. As a bonus if we can find high short interest and chart that represents a potential bottoming effect we've hit the sweet spot.

Enter AMBA

If you're not familiar, Ambarella is a developer of semiconductor processors for video that enable HD video capture, sharing, and image display. The company boasts a system-on-a-chip design that delivers audio, video, and system functions all on one single chip. Specifically, this chip design is great for wearable sports cameras (GoPro), auto aftermarket cameras, security cameras, telepresence cameras and UAVs (Drones). The company also has an infrastructure business for both professional and consumer IP.

AMBA is a former retail and Hedge Fund darling that sky rocketed with the ascent of $GPRO in 2015. This was a powerful beta play that rivaled returns of last year's darling $NFLX before it double topped out in July 2015.

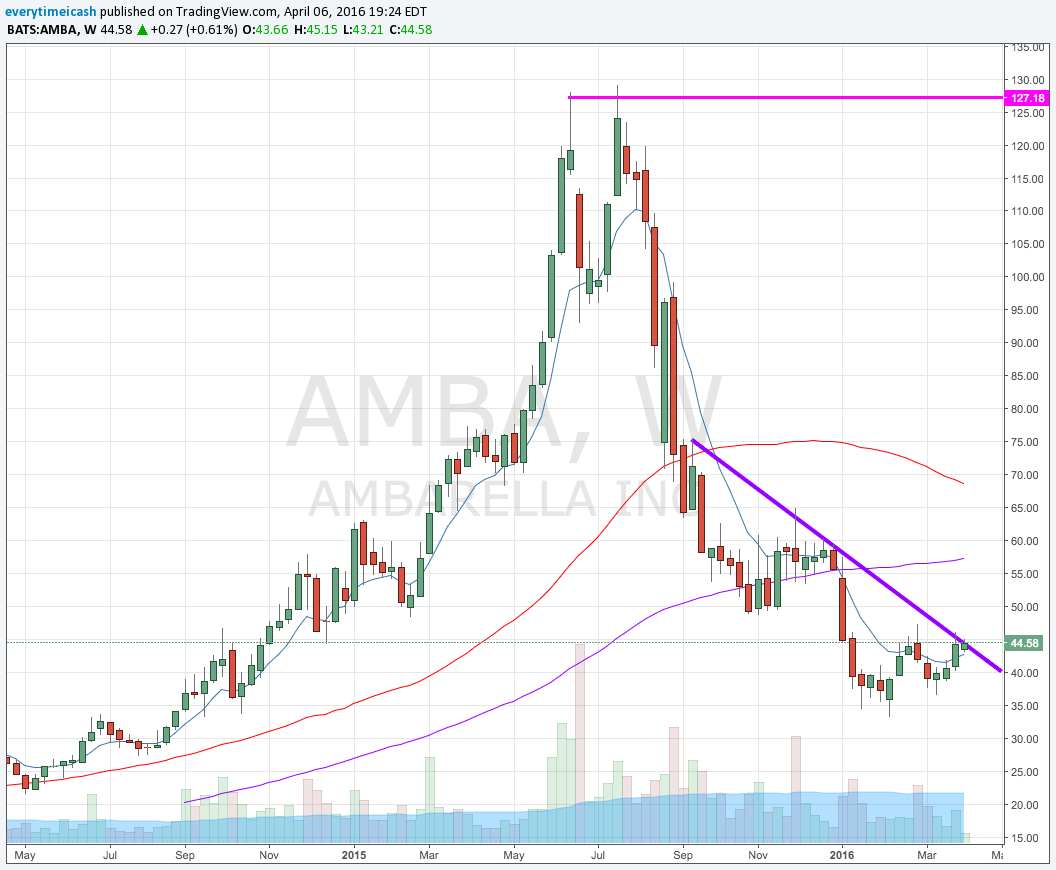

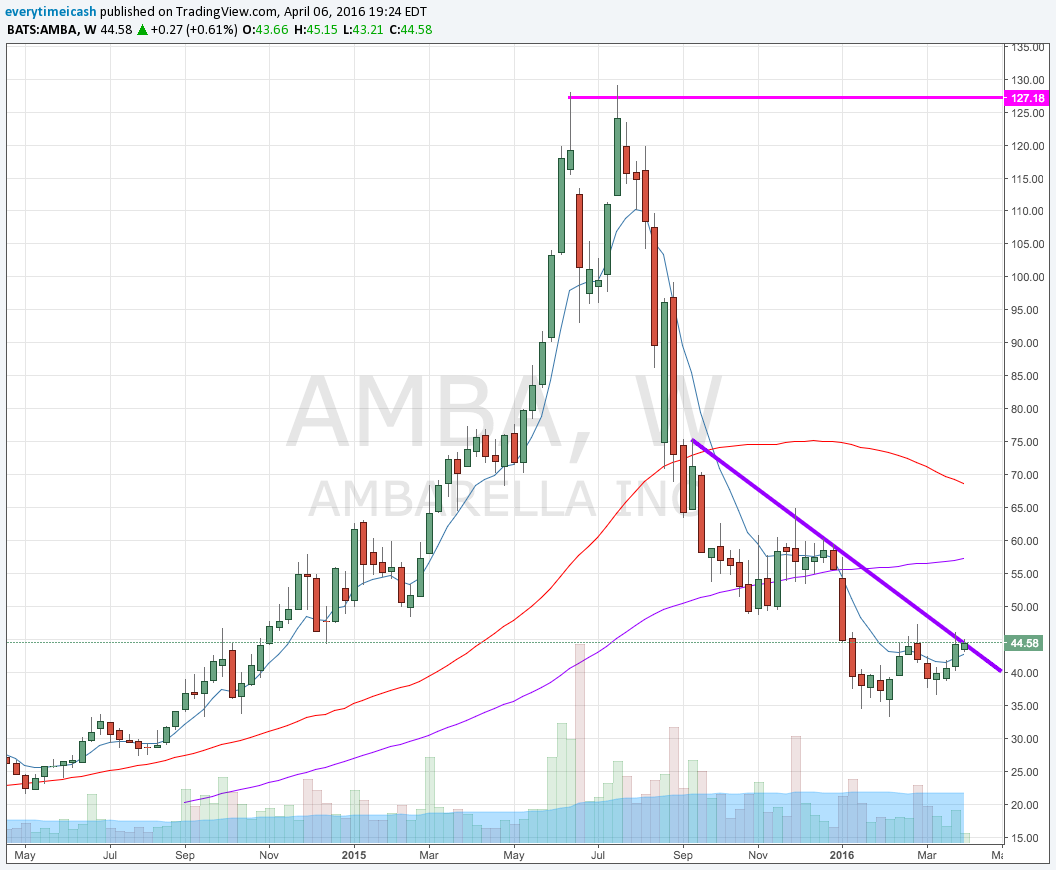

AMBA Double Top

If you lay a chart of both $GPRO and $AMBA over one another you'll notice that both issues have descended very similarly since July2015 until recently.

As the above two images illustrate, AMBA started to decay shortly after GPRO's sales numbers started to deteriorate starting in July. Since AMBA was so heavily levered with GPRO's business and since GPRO's management couldn't get anything right ever since Nick Woodman bought his yacht, the stock slid precipitously in tandem with GPRO.

That said, the stock charts seem to suggest a potential decoupling has begun occurring and with this former high flyer having fallen out of favor it's time to look under the hood.

Beam Me Up

With the recent consolidation in the space, none larger than AVGO and BRCM, it seems that the entire semiconductor space is in play. With that being the case, let's discuss some of the reasons AMBA is an attractive target.

FIRST AND FOREMOST, AMBA BOASTS A MIRACLE WITH NO DEBT TO SPEAK OF.

I want you to let that statement sink in a moment, this is a company that makes chips powerful enough to man audio and hd video on everything from handhelds to drones and smaller than a quarter, yet has no debt to speak of in doing so.

Cheaper than Peers on Forward PE and SOLID margins in both gross and EBITDA

As we stated above, AMBA has no debt to speak of and it's currently cheaper than it's peers (who have debt) and boasts strong forward growth and margins.

Specifically, EBITDA are the highest levels they've been at in six years.

Revenue Growth

45% YoY revenue growth to speak of actually. Now, granted, this is the area that catches the most flack because of their relationship with GPRO. Having said that, every piece of technology is getting smarter and again with no debt on the balance sheet it's not difficult for the company to shift their focus from GPRO to something more lucrative. Furthermore, one of their verticals is set to explode soon (Drones).

This revenue growth is impressive as fuck. It is only trumped by MXL and IPHI but that is predominantly due to acquisitions done on their part.

THE BAD

As I stated earlier, this company's handicap came at the hands of their partnership with GPRO. Specifically, their margins last quarter fell to 14% from 27% in Q4. Other quarter comps set at 30% previously. This could potentially represent the buying opportunity investors are looking for moving forward.

FUN STUFF

This stock has boasted a 53% institutional ownership for quite some time. Remarkably, even with the descent in share price, investors have not jumped ship. The stock has maintained its nearly 54% institutional ownership with Vanguard being the largest shareholder.

Shortly after July the stock's short interest peaked and has held steady since. Recently however, it appears that there is a convergence that has begun between short interest and price. This is a very bullish sign and a "reversion to the mean" is likely to occur.

And now, my favorite parts:

AMBA currently has ~35% of its stock short. It also boasts 53% of its float owned by institutions that have held through this downtrend. Most importantly, ~86% of the current available float is short. This is a recipe for a potential massive short squeeze.

AMBA Ownership Details

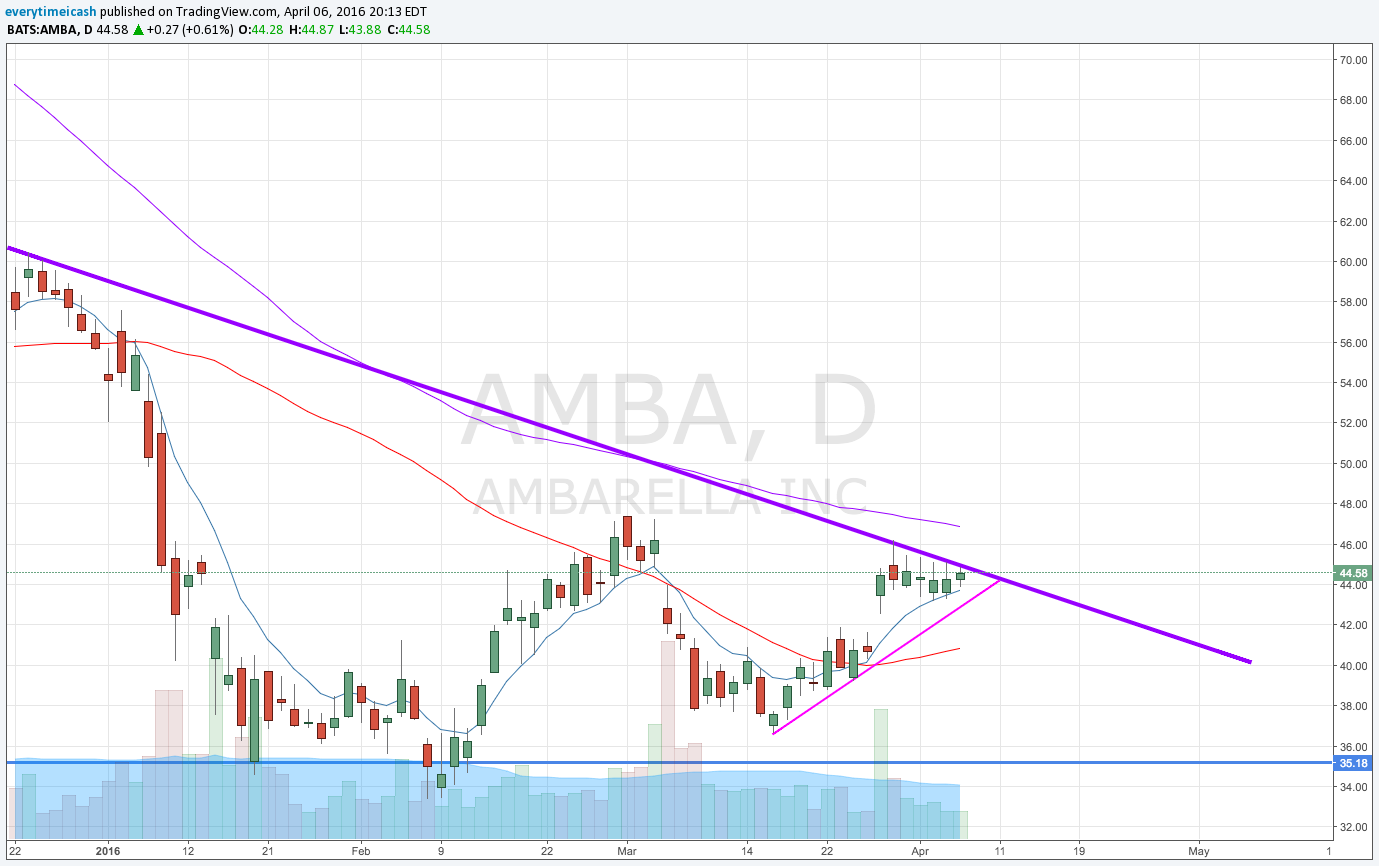

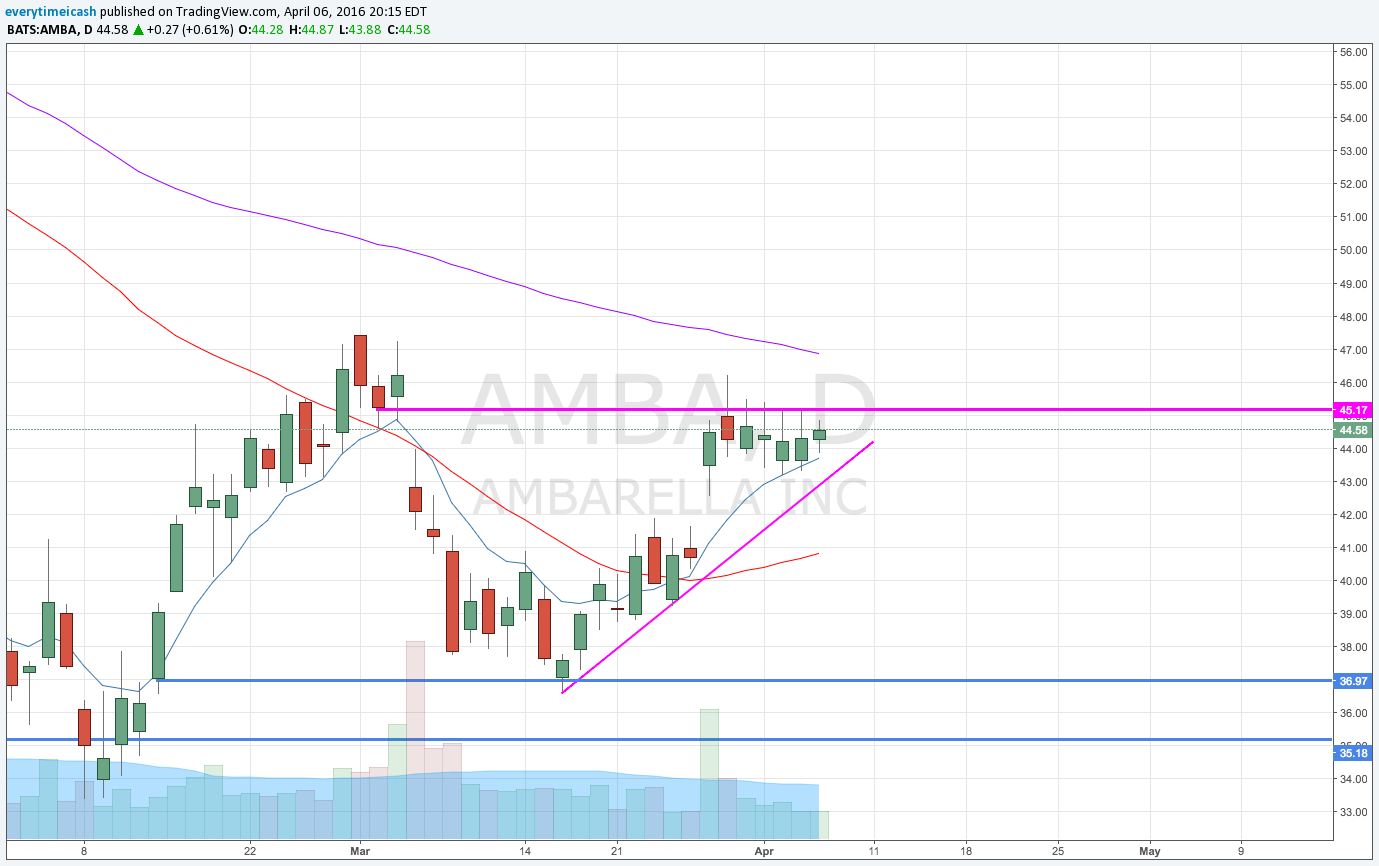

CHARTS

As the charts show above, AMBA recently created a higher low on the Daily charts and is currently consolidating in a tight bull flag that is pressed up against its downtrend that started back in September. We also have a bullish crossover occurring on the daily chart and a rounding 8 and 13 on the weekly. With 35% short and a constructive base forming, this stock is setting up for a potential run to 60+.

CONCLUSION

With high short interest, no debt, great YoY growth, decoupling from GPRO chart, base building on multiple time frames, and a large institutional ownership group AMBA is a buy. With IV cheaper than ever in this name, it would be prudent to look at using Calls as a leveraged way to get behind this stock. If consolidation continues in the space this name should be a prime candidate with a potential 27% upside premium (by my math). Aside from that, the basing charts, and the dash for trash pose a great setup for those that are interested only in trading the name.