Key Points:

The Red Flags are there, but is there a pent-up spring that could first uncoil?

Sentiment data is back to neutral after a bearish extreme

Technicals

The consensus around low-inflation and low-growth is so complacent it’s time to look the other way

The market has been in a familiar quandry in recent weeks with macro themes consistently stoking fear and keeping sentiment data in check, but asset prices holding up better than you’d imagine given the level of pessimism that appears systemic.

In the past, and during the course of this market bull cycle, we have seen this type of scenario play out to upside breakouts once uncertainty drivers resolve on some level.

The large timeframe pattern in the S&P 500 plays well for that type of resolution once again, with a bullish ascending triangle pattern seemingly coming to a head around a rough 3000-level trigger zone after months of feeble attempts by bears to sell the market.

Keep that in the back of your mind — cyclical bear red flags have sprung during recent months, reflecting very large timeframe warning signs that may still ultimately have the last laugh following a breakout.

Coiled Spring?

Economic weakness in US data has been mostly driven by manufacturing indicators/data and can easily be linked to concerns about the global supply chain. This of course comes on the heels of a world where we are seeing an accelerating decoupling between the US and China.

But much of what we have seen is a psychological, narrative/headline driven process based on deteriorating rhetoric between the US and China during the last six months. At least, that’s how it stands to look from the outside.

Soft vs Hard Data (Source: Briefing and www.sentimentrader.com)

One could speculate that we might see an active effort by the White House to firm up confidence by a strategic shift in rhetoric and narrative framing from now until the election. We have already begun to see that with the clearly optimistic pony show in the form of a “Phase One” China trade agreement supposedly on track.

In this hypothetical, given that other data sets such as retail sales, housing, consumer confidence, and employment have yet to show weakness another strong leg to the cycle is certainly possible. Cautious attitudes and actions in the industrial and transports subsets of the economy (in terms of business investment, as detailed by the Fed in both Minutes and Beige Book), despite maintained consumer confidence, spending, and jobs, could spawn a "pent-up business investment" type of narrative searching for an excuse to flourish against consensus expectations in the quarters ahead.

I am of the bias that you will see encouraging statements/gestures made to the markets and global business leaders responsible for the strength of the economy. Trade War rhetoric will be more tempered down, and in some cases positive. De-escalation will likely take fold during this upcoming campaign cycle.

On the extreme positive front, we may even see the White House try to temper fears with a new narrative that allows for reduction of tariffs. This type of action can put tariffs as a functional policy tool for the US economy. Trumpito and his cronies can ramp them up when they are less concerned about US leading indicators, and walk them back down when they want to fuel more growth and confidence. If you’ve paid any kind of attention, this is already taking fold and is becoming more and more developed over time.

It is obvious that there is already some understanding of these basic relationships in the oval office at this point. And there will likely be growing pressure to effectively use the "tariff/trade war rhetoric" policy as a stimulus source. Remember, the goal for this administration in the coming year is to win re-election. Historically speaking, re-elections do not take fold when there is a poor economy. So just on that basic level alone, improving domestic economic confidence by conveying confidence around resolution and by finding a workable narrative framework for reducing tariffs is the gas needed to keep this punch party flowing.

In simpler terms, it may be a predictable notion that the White House is incentivized to use its control over the

”Trade War” theme as a lever to guard against economic weakness and to promote improving economic data over the next 12 months.

This doesn’t mean that things will be easy to manage.

This big question then comes down to the following:

Is it too late? Is the economic downturn already in full effect and reached the inflection point of no return?

Will the markets and corporate America actually believe the White House when they attempt to spin the Trade War into a positive? The White House has lost a lot of credibility by over-promoting (lying about) recent achievements, inflecting on major issues without warning, and by creating chaos in some cases)

Will China play along? Whether or not you want to believe it, China is in fact in charge. They can decide whether or not they want more Trump simply by rejecting and discrediting him/his administration in the next 12 months should they not want to “play ball” with the administration.

Technically Speaking

The only persisting trend that has existed in the last several years has been the divergence between the US and the Rest-of-World (ROW).

Inside of that narrative, the immediate technical context for the US equities market is a relative narrow range in place since July. But it features a clear Bullish Ascending Triangle.

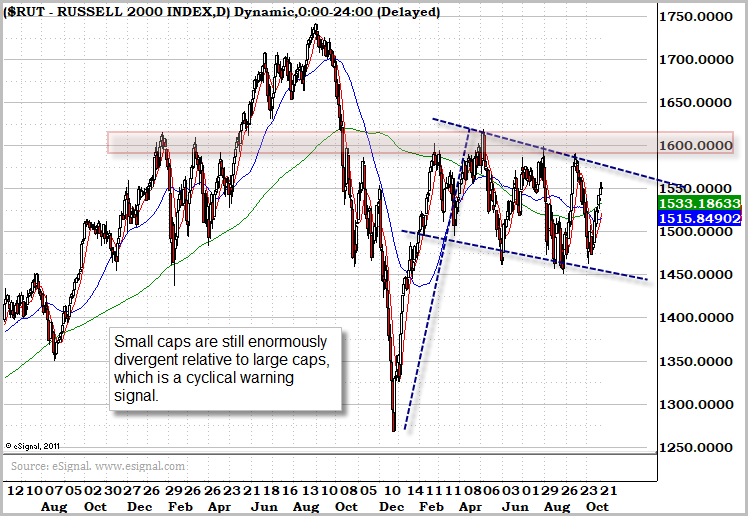

Based on other factors, including, but not limited to, bull flags in the Russell 2000 Index and the Dow Jones Transportation Average, but also the fact that those flags come in the midst of very clear -- and cyclically bearish -- divergences with the S&P 500 Index and Dow Jones Industrial Average. I am of the belief that we may be setting up for something similar to what we saw at the end of the 20th century with a blow-off run above 3000. Before I detail the generalities I want to point out that the markets are up around 50% since the election. There is no bigger talking point for Trump than a statement such as “The markets have doubled since I was elected.”

With that said, respectively, you can imagine something like a blow-off top run on a breakout of 3000 that would ultimately reverse sharply after irrational exuberance is met with a decay in the underlying sentiment. Or until the powers at be run things too hot and the kerosene fire just gets too hot.

Below you will see an assortment of charts that will illustrate to you the aforementioned scenario.

Source: Briefing

Sentimental

Personally, I primarily use sentiment data as a mechanism to field a grasp of where things lie. I don’t use it as the major indicator for why I put things on. However, it is important to note that stock markets are just a function of human behavior contextualized into data sets.

With that said, data suggests that options have been moving back towards neutral after hitting extreme pessimism and bearishness in the last several weeks. This reversion likely comes on the heels of “improving” data (hard data), the sentiment shift in “trade deal” status, and the simple “risk on” action taking place in the markets with both the Fed put and the softening trade war.

When you take a look at longer term data factors, Margin Debt is lagging the recent rally. This means that debt used to buy equities is stalled which historically has been a bullish sign for markets that are not selling off. Simply put, people are not getting ahead of themselves to be long the market, and bears had every reason to sell the market and could not. The margin debt is a sign that people have not gotten aggressive and have been conservative. This conservative notion suggests that positioning is not full and that there is a “wait and see” approach in the markets. This sets up for an “offsides” when it comes to positioning and a potential to see a chased rally outlined above in the event that the markets break out. This chase will especially be escalated if it is aided by the help of macro data and/or policy shift to a more positive situation.

Offsides, Defense

For the last 18 months, or so, this market has been defined by crowded ideas that have investors offsides. The four most dynamic moves since January 2018 in the market have come on exaggerated offsides consensus views (both up and down).

As we’ve seen, when a particular view on the world is agreed upon by just about everyone, it has the potential to have dramatic implications for asset prices far and wide if it turns out to be wrong. According to the latest BofA/ML Fund Managers Survey, only 4% of large fund managers believe inflation will pick up over the next year.

Taking note of this we want to look at positions that are crowded that could potentially generate some alpha should this consensus group think be incorrect. With that in mind, it is important to note that the following are true:

We have seen record inflows into government bond markets

We have seen negative yields around the world

We currently have the largest all time short build up in copper futures (CFTC Data)

When taking the above into consideration, it is important to note that this is the type of action that takes place when there is an aligned view that inflation is not going to happen. This type of positioning is not taking into consideration the potential that the Fed trying to manage inflation expectations could go horribly wrong and that inflation could accelerate faster (as it often does) than anticipated.

The secondary elephant in the room when it comes to this notion is that Trump, and his administration, are stoking the coals for a potentially overheated marketplace with their demands that interest rates “should be significantly lower.”

On the surface the lack of concern for an inflationary period “makes sense.” Manufacturing indicators are struggling and many data points on inflation and inflation expectations continue to show no life. However, central banks have been trying to stimulate in places like the EU and Japan, as well as the US , India, Brazil, Australia, all of SE Asia, and parts of Africa. Basically anywhere that is not Canada is trying to stimulate. Despite all this stimulation, like an old man with erectile dysfunction, economic data continues to disappoint.

Naturally, if you’re managing capital, you can feel apathetic about growth picking up too fast and driving an inflationary scare. It doesn’t look the least bit likely. This form of apathy often creates a set of complacency that we have been seeing in the last 18 months or so.

So now we must address the 800lb elephant in the room — What if it everyone turns out to be wrong?

As stated earlier, we may see a coiled spring ready to scramble into action if the current conditions softened more favorably as individuals have been reluctant to press the bullish note. With so much easing already in place, lending activity continuing to grow, and consumer confidence holding up quite well, the removal of the Trade War fears may prop open up the door to some aggressive “risk on” stances.

This attitude is something that you have already started to see. My service has been highlighting “bearish to bullish” reversals for about two weeks now and some of the biggest winners during that time have been these types of reversal trades.

Below we will take a look at some of the best setups in an environment like the above stated. (Source: Briefing)

Crowded positioning on the short side with copper futures sets up an unwind potential should this position break out of its downtrend. With CFTC data suggesting copper short extremes are in along with long end of the curve extremes on the bond front this is setting up for a dangerous Molotov cocktail for unwinding bonds and ripping copper and the like higher.

Refinance Bang

It is very important to remember that the above is coinciding with a more accommodative Fed. In this case, the easing in interest rates is setting consumers up for a refinance swoon that will ultimately end in horror as you cannot fix debt with exponential debt. In the intermediary however, it sets up the consumer for a belief that they are teflon. It also buys “zombie” companies who will eventually not be able to service their debt more time. In this event we could see a release of “animal spirits” once again in advance of the finality of all of this.

With that in mind, specifically, the action in bonds has sparked a reversion in the 3/10’s and a regression in the long end of the curve. This type of action bodes very well for the cyclicals and for banks in general. I will end this write up with a flurry of charts for names that “should” do well if this theory plays out as it very well may.

Firework Finale

If you liked this content please click the ❤️ below and/or share it!

TOTALLY FREE Trading Packet!

Click here to get my packet that shows you how I traded $600 into $100K FOR FREE.

This packet will explain to you in depth how I trade and how I manage my risk.

I am happy to share this. Just use the code KPAKFRAUD at checkout and you will get it TOTALLY FREE. You will pay absolutely nothing.

SHAMLESS PLUG

Check out the latest episode from my podcast below.

If you'd like to follow my trades in real time click the "Join Now" button at the bottom of the page. For those that will and have asked, use the code 1ST on checkout for a discount with no commitment beyond one month.