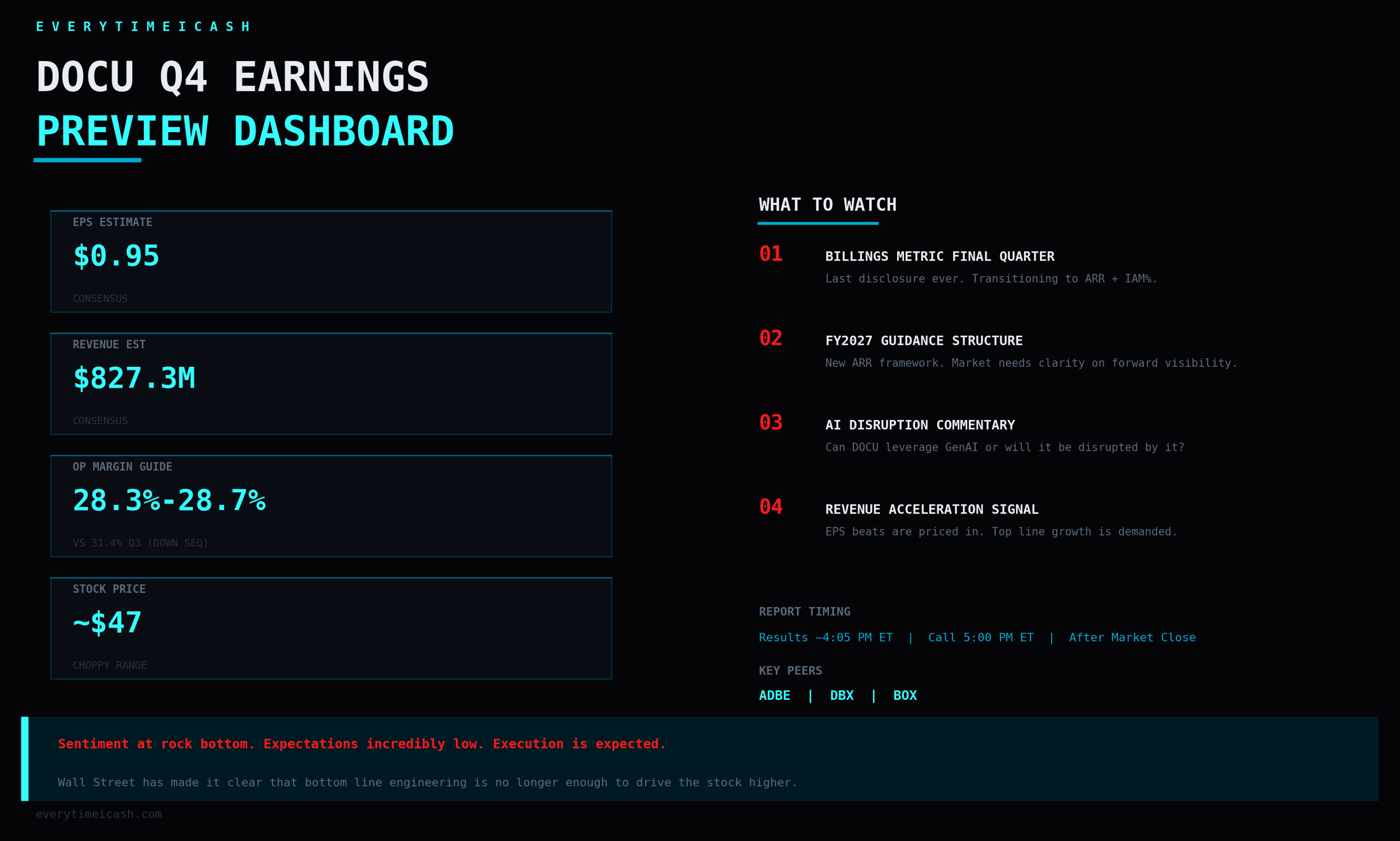

DocuSign is scheduled to report its fourth quarter results today after the market close, typically releasing the numbers around 4:05 p.m. ET, with a conference call to follow at 5:00 p.m. ET.

The consensus projects an EPS of approximately $0.95 for the quarter, while revenue is expected to come in around $827.3 million.

As a leading provider of electronic signature and agreement cloud solutions, the company is fighting to prove it is more than just a pandemic era relic. The stock has been exceptionally choppy in recent months, currently trading near the 47 level, as investors weigh growth durability against rising competitive risks. Key industry peers include Adobe, Dropbox, and Box.

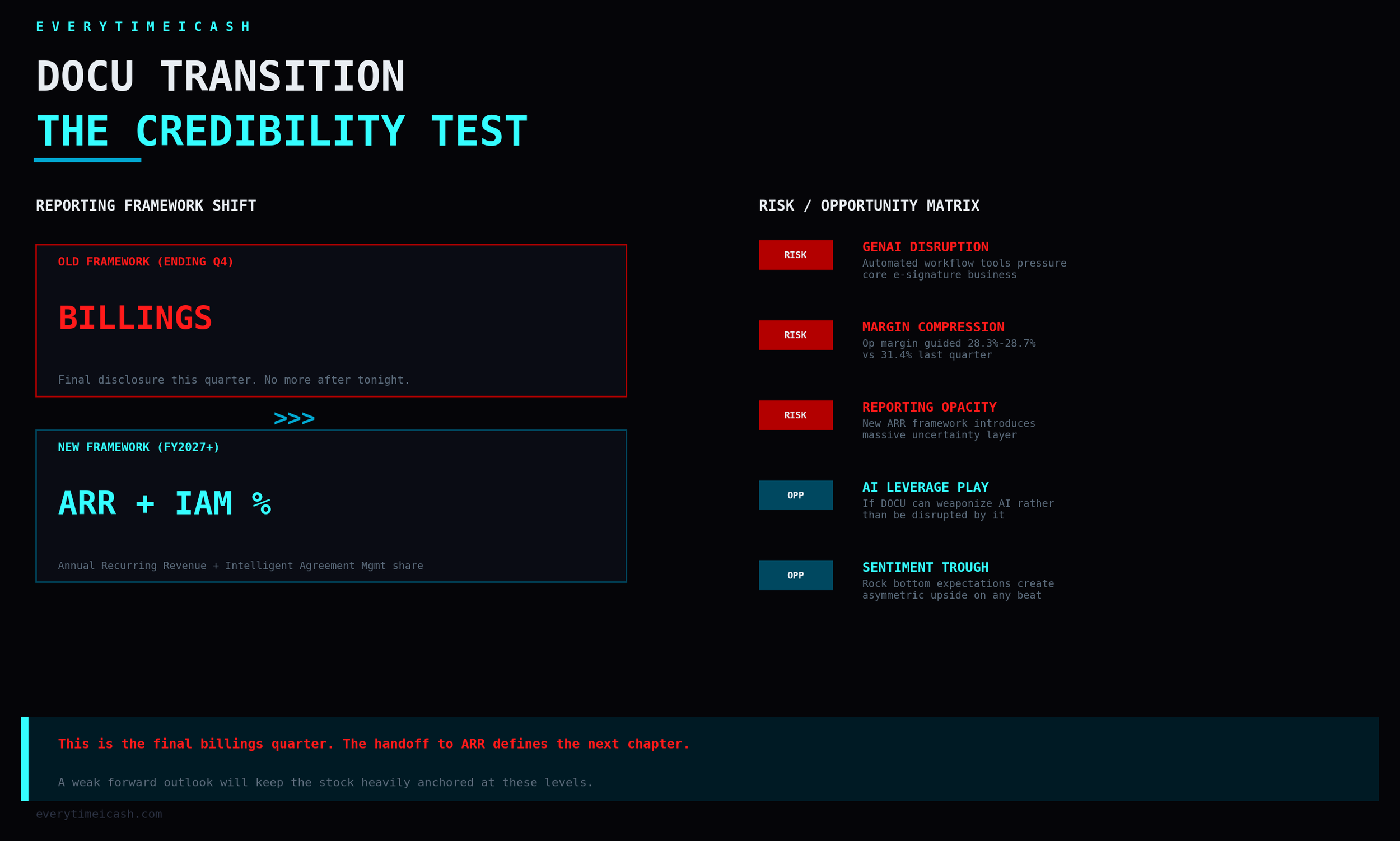

The transition in financial metrics is the primary thesis driver tonight. This fourth quarter marks the absolute final time DocuSign will disclose its billings metric. Moving forward into fiscal 2027, the company is shifting entirely toward Annual Recurring Revenue and will introduce Intelligent Agreement Management as a percentage of that total. This transition inherently introduces a massive layer of uncertainty. Investors will be hyper focused on this handoff, looking for clarity on how to accurately assess forward visibility and growth under the new reporting structure.

The artificial intelligence narrative and margin trends are where the credibility test lives. There is a very real fear on Wall Street that generative artificial intelligence and automated workflow tools could severely pressure the core electronic signature business over time. Investors will be listening closely for commentary proving that DocuSign can leverage these emerging technologies rather than be disrupted by them. Furthermore, the non GAAP operating margin for the fourth quarter is expected to slip to a range of 28.3 percent to 28.7 percent, down sequentially from 31.4 percent in the third quarter. Management needs to prove that profitability discipline remains intact despite the top line moderation.

ETIC 2026 ANNUAL PACKET ON SALE NOW CLICK THE LINK BELOW

TECHS:

Sentiment is hovering near rock bottom and expectations are incredibly low. The company has a strong track record of beating EPS estimates, but Wall Street has made it clear that bottom line engineering is no longer enough to drive the stock higher. The muted reaction to last quarter proves that execution is expected but top line growth is demanded. To spark a sustained reversal and break out of this choppy trading range, DocuSign must deliver convincing revenue acceleration and issue upbeat fiscal 2027 guidance that puts the artificial intelligence disruption fears to rest. A weak forward outlook will keep the stock heavily anchored at these levels.

If you liked this content please click the ❤️ below and/or share this post.

SHAMLESS PLUGS

TOTALLY FREE Trading Packet!

Click here to get my packet that shows you how I traded $600 into $100K FOR FREE.

This packet will explain to you in depth how I trade and how I manage my risk.

I am happy to share this. Just use the code KPAKFRAUD at checkout and you will get it TOTALLY FREE. You will pay absolutely nothing.

Check out the latest episodes on my YouTube above.