Current Quarter Expectations: As usual, operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Wolf's Den

Viewing entries in

Earnings

Current Quarter Expectations: As usual, operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Current Capital IQ consensus stands at EPS of $8.04 on Revenue of $20.77 bln.

Key Things to Watch

Capital IQ consensus calls for Q3 adj. EPS of $0.37 on revs +3% to $3.72 bln.

Capital IQ Consensus calls for 2Q16 EPS of $1.39 & revenue growth of 18.9%, compared to 2Q15 EPS of $1.23 on revenue of $2.28 bln.

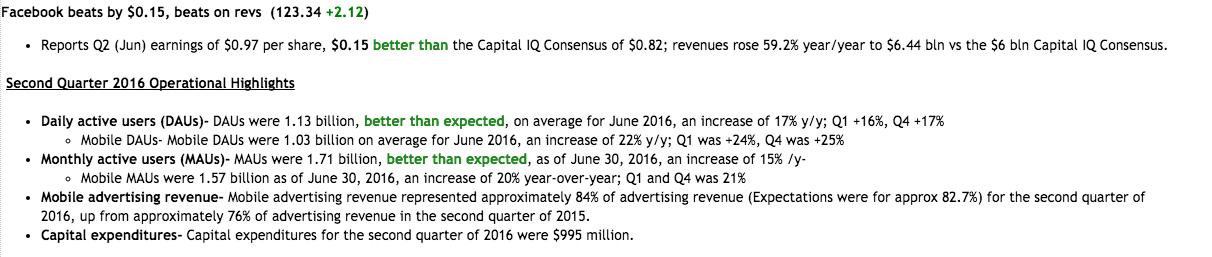

Current Capital IQ consensus stands at EPS of $0.82 on Revenue of $6.00 bln.

Q1 Recap

Analysts are looking for Q2 adj. EPS of $0.16 with adj. EBITDA +37% to $88.8 mln and sales +16.5% Y/Y to $296.8 mln.

Match guided for Q2 dating rev +4-5% Q/Q to ~$270.8-273.4 mln with a dating EBITDA margin in the low to mid-30% range vs. 26% in Q1.

Twitter (TWTR) is set to report Q2 earnings tonight after the close with a conference call to follow at 5pm ET. Current Capital IQ consensus stands at EPS of $0.09 on Revenues of $607.4 mln.

Q3 Capital IQ consensus calls for EPS of $1.39 (versus $1.85 last year) on revenue of $42.126 bln (-27% YoY). The current consensus is near the mid-point of the company's guidance of $41-43 bln.

The current Capital IQ Consensus Estimates call for Q2 EPS of $0.94 and revenues of $3.09 bln. VZ expects full year 2016 adjusted earnings to be comparable to the co's full year 2015 adjusted earnings of $3.99 EPS

Freeport-McMoRan (FCX) is expected to report Q2 results tomorrow before the market opens with a conference call to follow at 10am ET.

FY16 Guidance

The co reiterated FY16 guidance below Consensus on April 28 when they reported 1Q16 earnings. Capital IQ Consensus calls for a 2.5% decrease in FY16 rev to ~$31.8 bln, compared to $32.6 bln in FY15.

1Q16 Recap

Technical Analysis

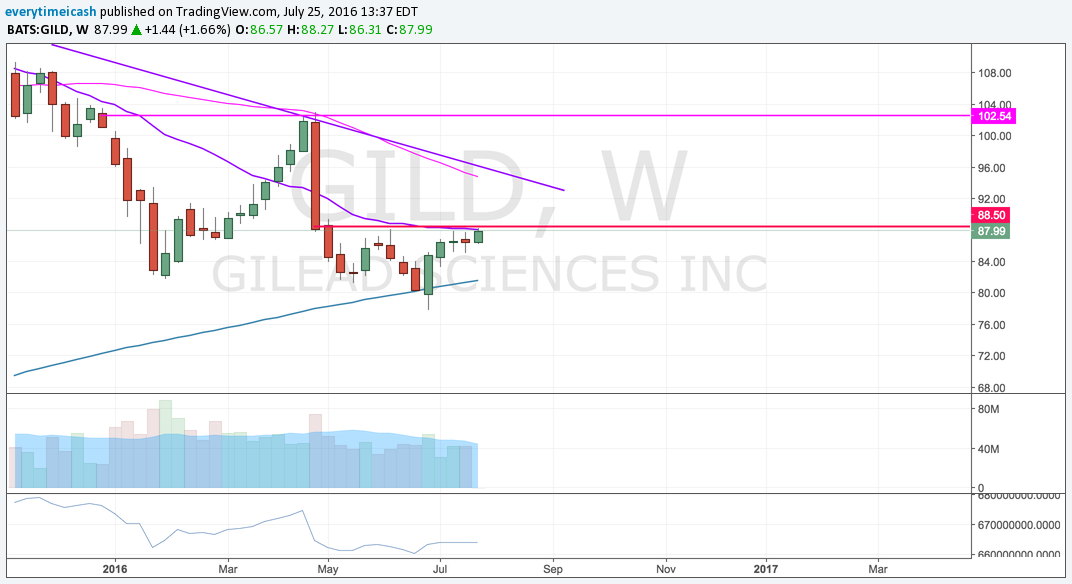

Technically, GILD has been an under-performer since its last earnings report in April had its selling back down to its early Jan/Feb lows around the $82 area. Buyers will want to clear this 87/88 resistance and lift price back into the late-April bearish gap between the 92/96 zone.

Based on GILD options, the current implied volatility stands at ~ 29%, which is 14% higher than historical volatility (over the past 30 days). Based on the GILD Weekly Jul29 $86.5 straddle, the options market is currently pricing in a move of ~5% in either direction by weekly expiration (Friday).

Last quarter, Under Armour beat Q1 EPS estimate by $0.02, reported revs in-line, guided Q2 operating income / revenues in-line and slightly raised FY16 guidance / reaffirmed margin guidance.

Headed into the print: UA has held onto these recent gains and is back near pre-Q1 levels.

Based on UA options, the current implied volatility is 14% higher than the historical volatility (over the past 30 days). UA Weekly Jul29 $42.5 straddle is currently pricing in a move of ~8% in either direction by weekly expiration (Friday).

Key metrics and areas of interest:

Techs:

Close to 40% of the S&P 500 will report their quarterly results this week. That includes McDonald's, which will report before the open on Tuesday.

Current Consensus is calling for adj EPS of $1.40 on revenues +6% Y/Y to $13.2 bln.

Q1 Expectations: EPS of $0.37 vs $0.56 year ago on sales -4.3% y/y to $5.96 bln.

Investors are still nervous following the Q4 results which saw the stock sell off sharply after the co posted soft installations Q4 results and Q1 guidance.

The company was unable to address the concerns around an increase in financing costs. They did announce two new refinancing deals this quarter which helped ease tensions.

Consensus stands at a loss of ($0.59) per share on Revenues of $169.55 (which would represent a decline of 31% y/y).

Analyst estimates call for EPS of $0.03, Revs +31.2% y/y to $155.53 mln. Expectations are in-line with the company's provided guidance from their Q4 report for revenues of $154-157 mln.

For RIG, what matters most is the spending of oil explorers and producers. Capital spending for this group has been cut over and over again by many companies since last year, which hurts companies in the drilling and oil service and equipment industries.

For now, oil drillers are aiming to reduce costs to help try and weather the oil slump. But there may be a little relief as the oil rig count, as measured by Baker Hughes (BHI), is expected to bottom in the second quarter.

The most recent weekly oil rig count data, released last Friday, showed that oil rig fell for a sixth consecutive week and are now down at levels not seen since 2009.