Celgene (CELG) will report Q4 results tomorrow before the market opens with a conference call to follow at 9am ET. CELG is expected to report Q4 results at 7:30am. Current Capital IQ consensus stands at EPS of $1.60 on Revenue of $3.02 bln

Wolf's Den

Viewing entries in

Earnings

Celgene (CELG) will report Q4 results tomorrow before the market opens with a conference call to follow at 9am ET. CELG is expected to report Q4 results at 7:30am. Current Capital IQ consensus stands at EPS of $1.60 on Revenue of $3.02 bln

IBM (IBM) will report Q4 results tonight after the bell with a conference call scheduled to start at 5:00 p.m. ET. Usually, IBM reports within the first 10 minutes after the bell.

NFLX had an aggressive International build in 2016. It also increased investment in its original content after so many of its shows (House of Cards, Orange is the New Black, Narcos, Stranger Things, etc) performed so well. The investments were complimented by a price increase that was 75% complete at the end of Q3.

Subs will remain topic of focus but investors want to see the company deliver. Especially with Forward P/E at a 145x 2017 earnings. The cash burn in Q3 was $506 mln and NFLX said it expected Q4 to come in at a similar level.

Domestic Streaming

International Streaming

NFLX SET TO TAKE OFF

Einhorn really put a damper on this stock yesterday as it confirmed an all time high breakout. It seems everyone from Carl Icahn to Einhorn want to take a shot at calling a top in this stock. "Valuation" is the obvious key concern for these guys, but it's all relative to how you value the stock. Take Amazon for example, it has been shot against on valuation for years now. That short selling and top calling has done nothing more than fuel Bezos' land buying spree.

NFLX has started to break out of a two year range and has cleared enough room for further upside. I want to play to capture that upside.

Excerpts from Shareholders Letter:

NFLX Key Metrics Courtesy of Briefing

Gigamon dives -18% on guidance; trading down near $38 after-hours. Next major area of support near June's breakout. This could be a foreshadow for darling stock NVDA IF they ever miss/soften their guidance.

The market will be paying close attention to several reports from the banking industry on Friday morning. The two "most important" being Bank of America and JP Morgan.

Shares of FSLR are holding steady at the $40 level ahead of the report. Shares hit a 52-week low of $33.74 on September 20 and are up over 20% but buyers have been unwilling to move in above the $40 level. The company needs to show it is meeting the worries about 2017 head on and that the concerns in the markets are overdone before it can press back toward the $50 level. This stands as a key quarter for the company.

Based on FIT options, the current implied volatility stands at ~ 75%, which is 64% higher than historical volatility (over the past 30 days). Based on the FIT Weekly Nov04 $12.5 straddle, the options market is currently pricing in a move of ~12% in either direction by weekly expiration (Friday).

Technically, FIT has been in a range for the better portion of this year. It found support in Feb and June with each probe of the $12-level, but also struggled to maintain strength above the $16-area.

FY16 guidance

Techs:

GILD has been in a slump throughout 2016 as it sits down -26% YTD near the $73-area. The path of least resistance remains to the downside as price flirts with 2-1/2 year lows & its down-trending 50-day simple moving avg near $77.

Options Activity

Based on GILD options, the current implied volatility stands at ~ 33%, which is 67% higher than historical volatility (over the past 30 days). Based on the GILD Weekly Nov04 $74 straddle, the options market is currently pricing in a move of ~5% in either direction by weekly expiration (Friday).

Gilead Sciences misses by $0.09, reports revs in-line; reaffirms FY16 (Dec) revs in-line

GILD notes they have seen 'strong adoption' of TAF-based regimens where they received reimbursement

Anticipated Milestones:

Guidance

Q2

FY17

Options Activity

TECHS:

Last week's downgrade took the wind out of the stock. Sellers responded with an aggressive drop below its rising 50-day moving average which has price in "no-man's land" ahead of earnings. Next key support is the 200-day simple ma near 73.

Shares of GOOGL hit an all time high of $838.50 on Monday but we have seen some profit taking ahead of tonight's report as the stock has pulled back to $820. The company is coming of an impressive Q2 in which it was able to accelerate revenue growth to over 20% for the first time in three years.

The growth was driven by Google website revenues as strength in the mobile and YouTube segments provided a boost. The rise in mobile has also boosted the growth in partners and website TAC which will be an area to watch.

The all time high will certainly be in play, especially when one views the Forward P/E of 20.5x being reasonable for a co that is posting 20%+ revenue increases despite being a $20+ bln a quarter company, no easy feat. A miss by GOOGL should prove interesting with the $783.50 Post-Q2 results being a key level of support. A break of this will send the shares to the $760 with the 200-sm ($757.29) in play.

Key Metrics

Q2 Recap

GOOGL reported Q2 (Jun) earnings of $8.42 per share, $0.38 better than the Capital IQ Consensus of $8.04. Revenues rose 21.3% year/year to $21.5 bln vs the $20.77 bln Capital IQ Consensus.

GOOGL/GOOG beats by $0.46, beats on revs

The company announced an oil discovery in offshore Nigeria; potential recoverable resource of between 500 mln & 1 bln barrels of oil. Some color about this find was in the press release. Color on this tomorrow will be good.

In other news that just came out a couple of hours ago, Exxon Mobil is mulling setting up a full-scale trading division, according to the FT.

XOM Chart: https://www.tradingview.com/x/ceKwvDIR/

Peers include: PTR, EC, TOT, SNP, STO, E, OXY, SSL, MITSY, ECA, YPF, PZE, RDS.A, BP, CVX

For Q3, the Street is expecting Q3 comps to decline by 18%

The company is still seeing the impacts of the E Coli crisis which negatively impacted comps and earnings.

PEERS TO WATCH: JACK, PNRA, BWLD, DPZ

In the Q2 earnings release, co lowers FY16 EPS to $6.10-6.30 from $8.15-8.35 vs. the $8.50 consensus; reaffirms FY16 revs of $93-95 bln vs. the $93.84 bln Consensus; reaffirms 740-745 commercial airplane deliveries but lowers operating margin to 4.5-5% from 9%.

BA was initiated with an Outperform at Robert W. Baird; tgt $161. Firm believes the FCF dynamic at BA continues to be underappreciated especially with $25 billion in FCF being generated during 2017-19 with ~$17 billion available for buybacks after dividends. Ramping build rates, seven-year backlog visibility with record low deferral rates, stable R&D costs, and productivity improvements lend to returning significant cash to shareholders. Their price target is $161 based on 11x their 2018 FCF estimate. Buying the pullback in BA shares as bear points priced in at current levels (October 6th).

Analysts have a consensus EPS estimate of $1.61 for the third quarter, which was $0.01 higher than their predictions of $1.60 90 days ago. Disney will report its third quarter results after the market closes.

The consensus estimates calling for a net loss of $0.07 per share on $169.82 million in revenue for the quarter. Yelp posted a net loss of $0.02 per share on revenue of $133.91 million in the same period of last year.

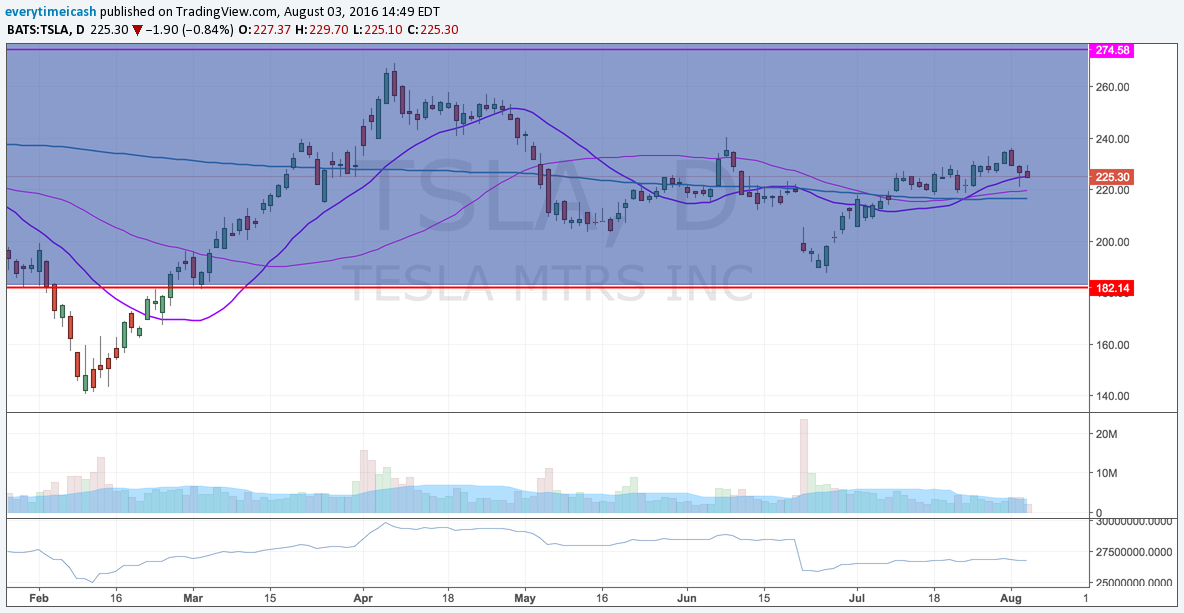

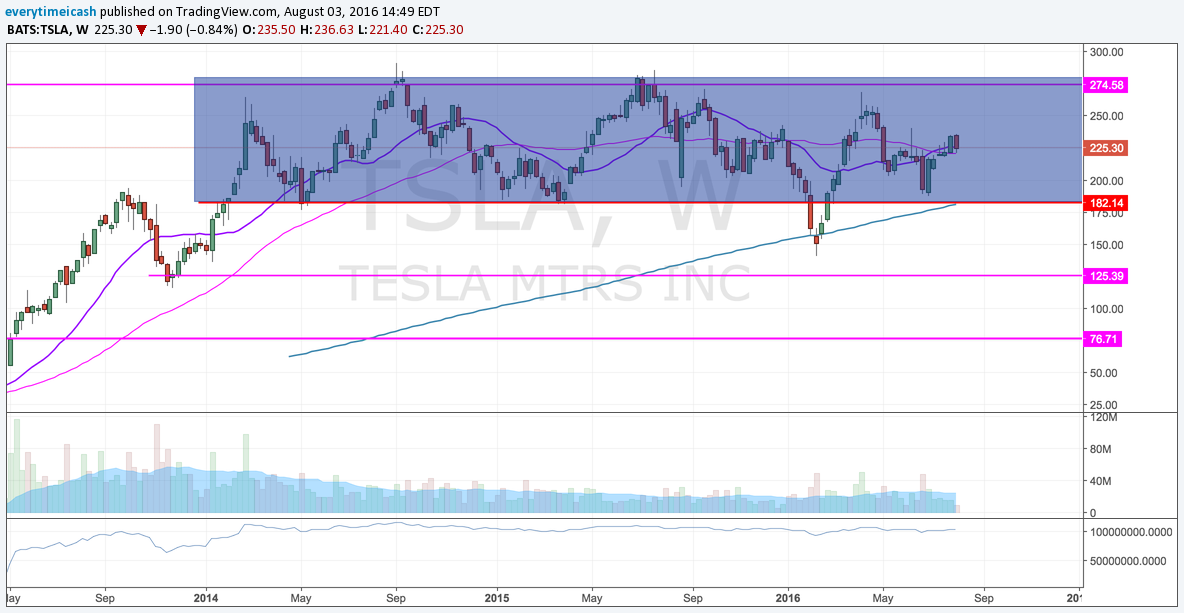

Tesla is expected to report Q2 non-GAP EPS of ($0.65) vs. ($0.48) last year with non-GAAP rev up 38% to $1.65 bln.

The stock has been very resilient despite added risks as investors give Elon Musk the benefit of the doubt.

Current Capital IQ consensus stands at EPS of $0.55 on Revenues of $862 mln.

The FSLR revenue recognition model makes it extremely difficult for analysts to provide accurate quarterly estimates. The company has been able to handily beat EPS expectations by an average of $1.03. Revenue has been a little less friendly with two big misses and three big beats over the past five quarters.

The annual projections remain the primary focus for the underlying health of the company and that is where we will be looking to judge the overall performance and outlook. Shares of FSLR have had a difficult 2016. The stock got out of the gates strong hitting a two year high of $74.29 on March 18. But the shares have tumbled 33% since that high water mark.

Shares of CAR have had a solid run since reporting Q1 results in early May. The co missed its EPS by 22 cents but revenues were in line and, most importantly, it guided FY16 revenue above the consensus. The primary driver, and what attracted investors, was commentary from the company that it was starting to see a turn around in the pricing environment for the troubled car rental business.

This stock fell from the $50 area in October of 2015 all the way to $22. So the recent upward trend allowed the stock to recapture approx 55% of its losses. But we are seeing the stock under pressure today as it has given up nearly 5% ahead of today's report. Shares are down approx 12% over the past week. This suggests that investors remain cautious on the name and are taking profits after buying low.

CAR will need to show a continued improvement in pricing to entice more investors into the name. It does have some solid support below at the 200-sma ($31.90) and the $33-34 area which both linger just below. Also we would keep an eye on Hertz (HTZ) which will trade closely with CAR on the news.

Key Metrics

Guidance

Q1 Recap