“There is nothing new on Wall Street or in stock speculation. What has happened in the past will happen again, and again, and again. ”

The fact that Wall Street repeats its same mistakes over and over again is nothing new. We are human and we are wired the same. If you're monotheistic religious believer or if you're just spiritual the fact greed and self serving is not a new concept to you when it comes to human nature. In religion this is seen early in the story of human creation with the story of Adam and Eve. In life, this takes form over and over again; especially on Wall Street.

The markets have seen a steady rise for the last seven years on the heels of the largest credit crisis we've ever experienced. Banks packaged loans and sold them to other banks which eventually cratered the basis of the economic system. Now we're starting to see similar patterns in the markets which are usually a 6-8 month foreshadowing of the general/broader economy. So our goal here is to figure out, is it over, did it just begin, or possibly something else.

CREDIT DEFAULTS

I am a believer that we may have the largest debt default in market history. That said, I want to talk about the pattern of defaults, specifically as the relate to corporate bond markets.

To put it simply, the cycle is usually like this -- Defaults on "speculative" bonds are <5% (basically less than 5% of non-investment grade US corporate bonds default in a year). When we break the 5% mark we (historically) get a three or four year rising, peaking, and then normalization. This is how a "normal" credit cycle usually works. It's healthy. People come up with ideas, turn into business founders, get money, go bankrupt. Rinse and fuckin' repeat.

Look back in time you see this cycle play itself out over and over again. (See below)

- 1990: Defaults pop from 4% to 8%. In 1991 they peak at ~11% then they decline reaching 6% in 1992. 1993, crisis averted and we go back to normal around 3%. About $50Billion in corporate debt goes into default

- 1999: Machine goes on H.A.M. again, default blast 5+% and then ramp through 2001 hitting 9ish%. Then they start to normalize around 2002 and everything back to normal in 2003.

- This time the junkies had much more debt than 1990. About 10x more -- $500Billion lost in default. This growth in risk was because of the love of the CDS market.

- 2009: Mortgage crisis starts stinking up every fuckin thing it touches. Defaults power to 10%. This time it was different though. The Fed steps in and stops the cycle dead in its tracks. "Too big to fail" become commonplace and inject some cash steroids into the markets.

- $1 TRILLION in debt goes into default (even with the Fed band aid)

Remember though, markets USUALLY go through this cycle where they default, peak, crash and fuckin burn then normalize. The weak die the strong survive and it's c'est la fuckin vie all over again. However in 2009 Uncle Ben and his cronies stopped this normalization process. They stopped it dead in it's tracks and allowed the weak to survive and prevented the crash and normalization. Because of that they "avoided" TRILLIONS of dollars of debt from finding its way back to normalization. They wrote that shit off like it never happened and started pumping money back into the economy, business as usual.

QUICK EXAMPLE

Let me give you a quick example of how you can relate the above mentioned "Fed injection". Think of a person that has a compulsive credit problem. They take out a card, start using the shit out of it notice it's running low so they repeat the problem. Eventually they run up like 7 credit cards and realize "Fuck, I can't pay this off."

In this example, if it were a normal situation this person would likely default on paying the cards off and probably file bankruptcy or get a second job and pay things down -- lesson learned though.

Imagine this person has a really rich mom/dad and that parent steps in and is like "Ok, I'll pay this off for you don't ever let it happen again." In this case the person never really learned how big their issue was and never really "fixed" the problem. Their parent (Fed) stepped in and paid off the debts and they went back to business as usual.

BACK TO CDS PROBLEM

Because we never had our "debt clearing" situation in 2009, the Fed basically pressed "pause" on the impending doom and gloom. Basically we got a weak recover and an economy that's still heavily leveraged and debt dependent. "Business as usual."

So because that debt never "cleared" or "flushed" out of the system, we face a catastrophic debt obligation the next time "shit hits the fan." The main question is

"When does shit usually go bust?"

If you look above, the credit cycle usually starts up 6 years after it normalizes. (1999, 2009). Let's count up the years since we cleared our debt obligati-- Oh shit, we'er on the sixth year.

In 2006 we had our best year for speculative corporate debt in recent history. Two years later, well you already know what happened. The best since that time was in 2014, and well we're now in year two since then. Let's examine the estimates quickly:

- High yield experts say "base-case scenario" is between $1.6 trillion and $2 trillion in high yield bond defaults.

Personally, I don't like the conservative estimates because, well, Wall Street is full of greedy fucking money addicts and CDS markets make the size more catastrophic then the base.

THE TELL

In the mortgage crisis, the first tell you had of anything going bad was the default of sub-prime housing loans. So, it goes without saying that we'll check the sub-prime loan market to see if anything sucks there first.

Without doing much digging, we learn two loan markets have ballooned since 2008; Student and Auto loans.

Let's focus on autos. Every other day you hear some talking head tell you about how auto sales are at peak and record levels. Did people have a bunch of money left over since 2008 and just decided to "treat themselves?"

Short answer: No. Auto loan origination has boomed on a serious drop in lending standards. Not surprising in this junk you find sub-prime lending to people with bad or zero credit and no income.

HOW'S THIS HAPPENING?

Without getting too bogged down with details there's only one simple answer to this; cheap money. The Fed's zero interest rate policy has opened the door for a swoon of raiders to capitalize on the creation and origination of cheap money bad loans. This cheap money gives auto loan originators an interesting dynamic. They basically get "fixed" retail prices and they have high variable costs. When the cost of capital is cheap they pioneer stellar results and when the costs increase they suffer immensely.

Just like the mortgage crisis, we have yet another issue of subprime auto backed assets. Auto ABS for short. (Emphasis on "BS") We now have more than $20B in subprime Auto ABS. These loans are packaged repackaged and grouped with tons of other loans adding "extra credit protection". The risks are offset with the belief in a "large number is less risky than a small number of loans."

Without going all "gloom and doom" on you with the ABS market I want to focus on GM. Just know that packaging debts over and over again, especially badly lent debts, is a shit idea and almost never goes well.

MURICAN CAR MAKER

GM is a low-margin auto manufacturer that is dependent on cheap money for the sake of their business model. In a low rate and high auto sale environment you would expect this stock to perform favorably. That has not been the case however as the company is heavily in debt and little cash flows have been spent on paying off governments and unions.

GM is also, one of the largest owners of sub prime auto loans. The other largest player in auto finance is Santander Consumer USA ($SC), That issue (SC) has already begun its woodshed beating.

All subprime auto businesses operate the same way. They maintain margins that make up ~3% of their loan books. That means if their funding increases marginally their profits are depleted.

GM pays 3% for the capital is uses and earns ~12% on the subprime auto loans it dishes out. After everything is all said and done, their operating margin is 3%. The main point to take away is the small size of the operating margins after all is said and done. Remember that at the end of the day GM has been the beneficiary of cheap access to capital. That cheap capital allowed them to make bad loans and take out more cheap access to capital and more bad loans. We're at a "Peak" in auto sales, have cheap cash available, and at the end of the day they make a 3% operating margin.

As the Fed increases interest rates, these already low operating margins will get wiped. Furthermore, loan losses are going to go through the fuckin' roof because of weak regulatory actions that make it more difficult for companies to be able to repossess cars.

GM, like other companies have found new ways to avoid "delinquent" loans on their books. They now offer customers the ability to defer their loans. I want to point out that many of these loans are subprime and already have a long life cycle (6-8 years in many cases). If we put this simply, you got a company that borrows cheap money, turns around and loans it out with a higher rate, then they allow the people borrowing that money that can't pay it back to put it on "pause." They then can avoid pointing to the toxicity of the loans and the books stay "clean." Yeah, that's not going end badly at all. 💣💣💣💣💣

Aside from this nightmare scenario, GM (financial) debt-to-asset ratio is 80%. As long as interest rates remain zero (which they haven't) GM can continue to pay off their debts. Now that the cost of borrowing capital has risen, their ability to repay their debts should suffer.

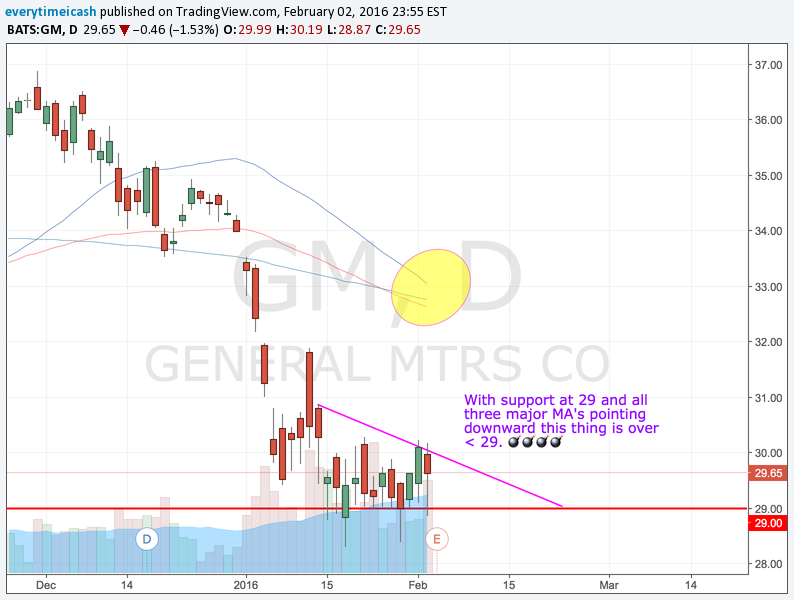

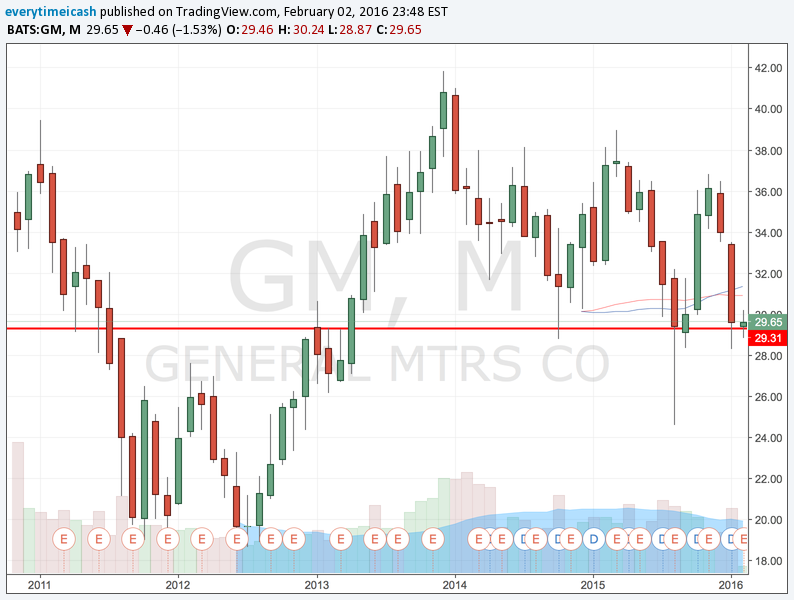

GET TECHNICAL

Even with access to cheap capital, peak auto sales, and a "lack of delinquencies" GM can't seem to arouse investors and perk its stock price. It's currently sitting at major support for the issue and it barfed to 20 the last time the 29 level broke. We want to short this piece of shit to the ground if that 29 level breaks.