Amazon.com (AMZN) is set to report Q1 earnings today after the close today followed by conference call at 5pm ET.

Current Quarter Expectations: Operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Prior Q1 guidance included: operating income of $100-700 mln, including $600 mln stock based comp, vs ~$550 mln estimate (initial estimates were slightly higher $650 mln); revs $26.5-29.0 bln vs $28.01 bln consensus. Incorporated into Q1 guidance: 130 bps from unfavorable FX (Q4 outlook assumed ~340 bps unfavorable impact from FX rates).

Q2 Guidance: AMZN will issue Q2 guidance for operating income (not EPS) and revenue. Current expectations are for Q2 op income of ~$850 mln on revs +22% to $28.3 bln.

Other 'Prime' Factors:

- Customer/seller growth metrics; discussed during the call

- Q4 Seller units/third party were 47% of paid units (46% last qtr) Fulfillment by Amazon or FBA units represented nearly 50% of seller units.

- Q4 unit growth metric was 26% (unchanged from prior qtr)

- Q4 active customer accounts was ~ 304 mln, up from 270 mln year ago (excluding customers who only had free orders, active accounts were 280 mln, up from 254 mln year ago).

- Prime: Q4 worldwide paid Prime members +51% y/y (+47% in US). Refrains from giving specific numbers -- but according to the 2015 letter to shareholders Prime has ‘tens of millions of members worldwide'

- Active AWS customers exceed 1 mln (last time AMZN disclosed this figure was Q4 prior year, when active AWS was ~1 mln.

- ChannelAdvisor data over the past three months has indicated strong growth trends. January SSS +17.8%, February SSS +16.6%, March SSS +14.9%.

- Prime growth / trends. Amazon does not disclose specific membership figures and commentary tends to be seldom and vague.

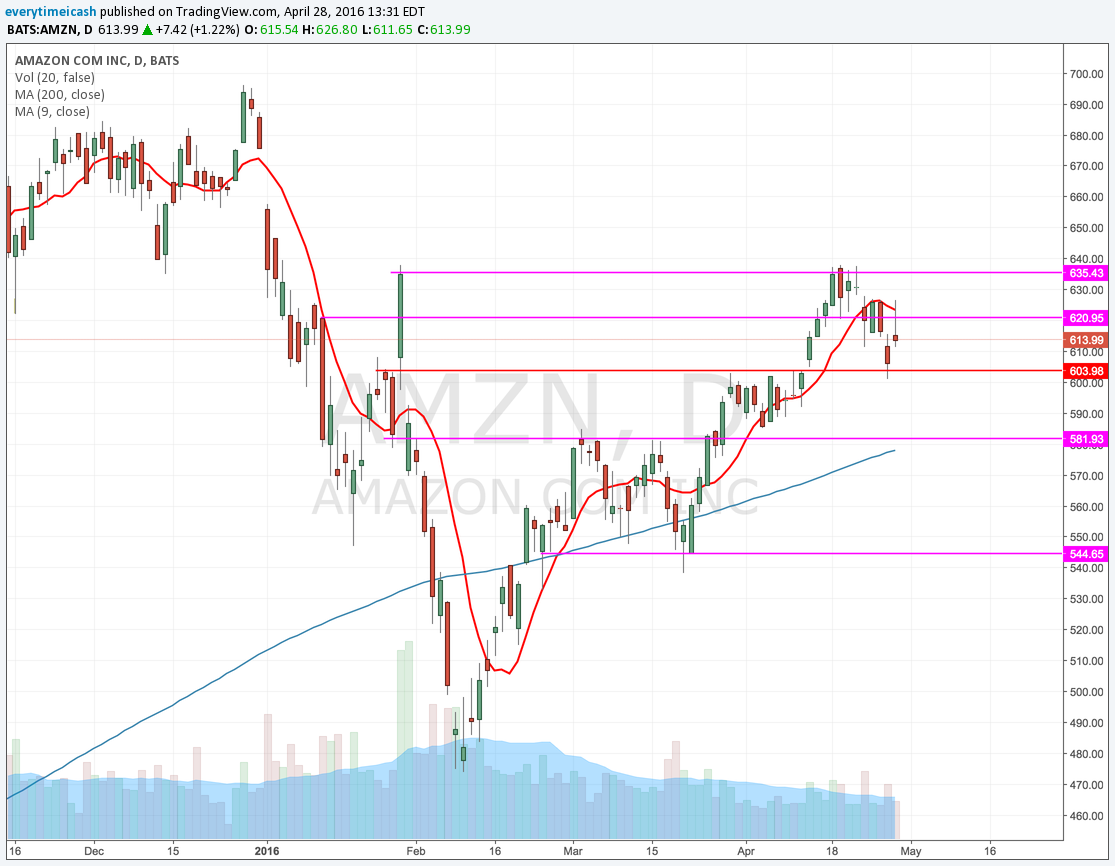

TECHS

Based on AMZN options, the current implied volatility is 2x higher than the historical volatility (over the past 30 days). The 1-day event volatility is more than 60 points (9%). That's really expensive, even for this name.

AFFECTED NAMES:

Retail - WMT (earnings May 19), ETSY (earnings May 3; AMZN competing service - Handmade service), BBY (earnings expected mid May), W (earnings May 9),EBAY (reported earnings April 26), BABA (earnings May 5).

Shipping - UPS and FDX (ATSG new partner).

FANG - GOOGL, FB, NFLX

Cloud - RAX RHT CRM CSCO EQIX BLOX QLIK GIMO BV BCOV ORCL TWOU QTWO.

RESULTS:

Amazon beats on the top and bottom line; guides Q2 sales midpoint above consensus, operating income in-line

- Reports Q1 (Mar) earnings of $1.07 per share, $0.47 better than the Capital IQ Consensus of $0.60; revenues rose 28.2% year/year to $29.13 bln vs. $28.0 bln consensus; operating income $1.1 bln vs. ests of ~$545 mln and $100-700 mln guidance.

- NA operating income +131% to $588 mln; net slaes +27% to $17 bln

- AWS operating income +210% to $604 mln; sales +64% to $2.6 bln.

- Co issues in-line guidance for Q, sees Q revs of 28.0-30.5 bln vs. $28.34 bln Capital IQ Consensus; operating income of $375-975 mln vs ~$850 mln estimate.

Amazon sees Q2 operating income of $375-975 mln vs ~$850 mln estimate; revs $28.0-30.5 bln vs $28.3 bln consensus

Amazon Q1 operating income $1.1 bln vs. ests of ~$545 mln and $100-700 mln guidance; rev $29.1 bln vs. $28.0 bln consensus and $26.5-29.0 bln guidance

This guidance includes approximately $825 million for stock-based compensation and other operating expense (income), net. It assumes, among other things, that no additional business acquisitions, investments, restructurings, or legal settlements are concluded and that there are no further revisions to stock-based compensation estimates.

Amazon now surges higher after-hours up towards 675 area; note the Jan bearish gap/December close at this 675 zone.

Now you see why Bezos is always laughing.

🚀🚀🚀🚀🚀