Freeport-McMoRan (FCX) is expected to report Q2 results tomorrow before the market opens with a conference call to follow at 10am ET.

Wolf's Den

Freeport-McMoRan (FCX) is expected to report Q2 results tomorrow before the market opens with a conference call to follow at 10am ET.

FY16 Guidance

The co reiterated FY16 guidance below Consensus on April 28 when they reported 1Q16 earnings. Capital IQ Consensus calls for a 2.5% decrease in FY16 rev to ~$31.8 bln, compared to $32.6 bln in FY15.

1Q16 Recap

Technical Analysis

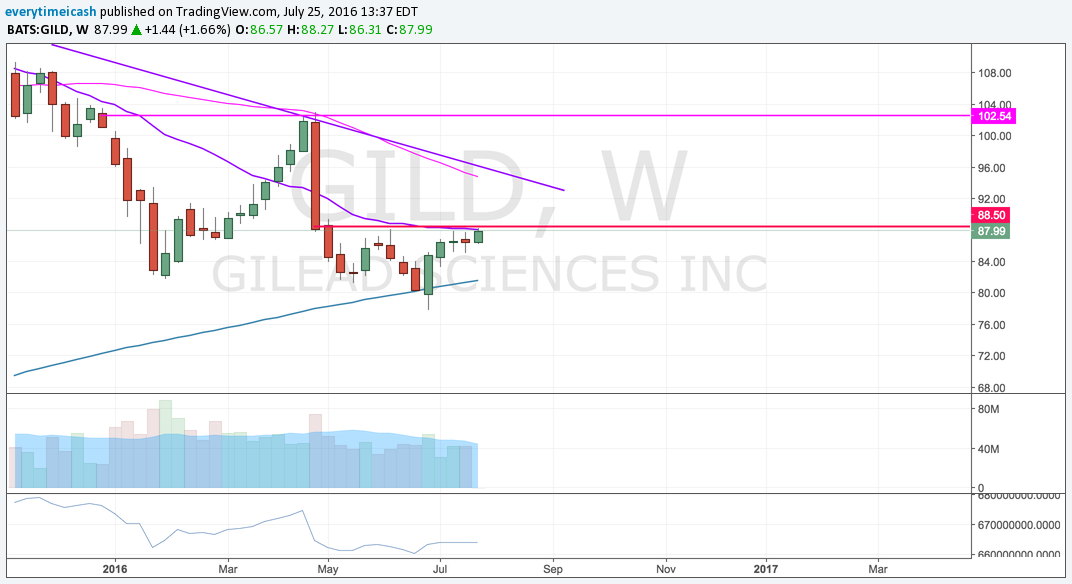

Technically, GILD has been an under-performer since its last earnings report in April had its selling back down to its early Jan/Feb lows around the $82 area. Buyers will want to clear this 87/88 resistance and lift price back into the late-April bearish gap between the 92/96 zone.

Based on GILD options, the current implied volatility stands at ~ 29%, which is 14% higher than historical volatility (over the past 30 days). Based on the GILD Weekly Jul29 $86.5 straddle, the options market is currently pricing in a move of ~5% in either direction by weekly expiration (Friday).

Last quarter, Under Armour beat Q1 EPS estimate by $0.02, reported revs in-line, guided Q2 operating income / revenues in-line and slightly raised FY16 guidance / reaffirmed margin guidance.

Headed into the print: UA has held onto these recent gains and is back near pre-Q1 levels.

Based on UA options, the current implied volatility is 14% higher than the historical volatility (over the past 30 days). UA Weekly Jul29 $42.5 straddle is currently pricing in a move of ~8% in either direction by weekly expiration (Friday).

Key metrics and areas of interest:

Techs:

Close to 40% of the S&P 500 will report their quarterly results this week. That includes McDonald's, which will report before the open on Tuesday.

As I've been telling you guys for months now, the rate increase is not likely to occur in June and most likely to occur in July. My rationale for this has always been two fold: 1) Brexit and 2)A rate hike now is too soon and one in September is too close to the election. Last week's data gave the markets a quick rattle but by the end of it investors and traders had been calmed by the depreciation in likelihood that the Fed would move in June. Well like a kid turning his homework in late, the market seems to be peeking over its shoulder at the Brexit event looming. With that, the market is pricing a lower possibility for a rate hike in June.

That said, we are sitting at 2100 with the potential of an all time high breakout in the stock market. My bias is that we will eventually take out the highs, continue to rally and cause capitulation before ultimately falling apart. So for now, the pain trade remains to the upside until a catalyst occurs to "shake things up". With that in mind, I'm focusing primarily on stocks that are poised for higher. Below are the SPY charts to keep an eye out including a FIBS chart for potential resistance.

Winner winner. 717 support.

Could be at support retest, could be a cup and handle, could be a rollover. It all depends on how 97.5 will hold.

Support retest held. This should be a long so long as this holds. Rising MA's should push this higher moving forward. 100.30 is the breakout.

Heavy short interest, zero debt, channel break, and now an issued buyback. This should catch gas to the flames soon and continue its way higher. Read this post if you are interested in swinging this name and/or want more details.

This name is itching for a breakout. Here is your level.

Flagging with 112 as support. Look for continuation.

Backtest of the breakout. Ready to rip again.

Strongest sector on the board at the moment. After months of consolidation, this sector is set to go. This one may get extended quickly so tread lightly.

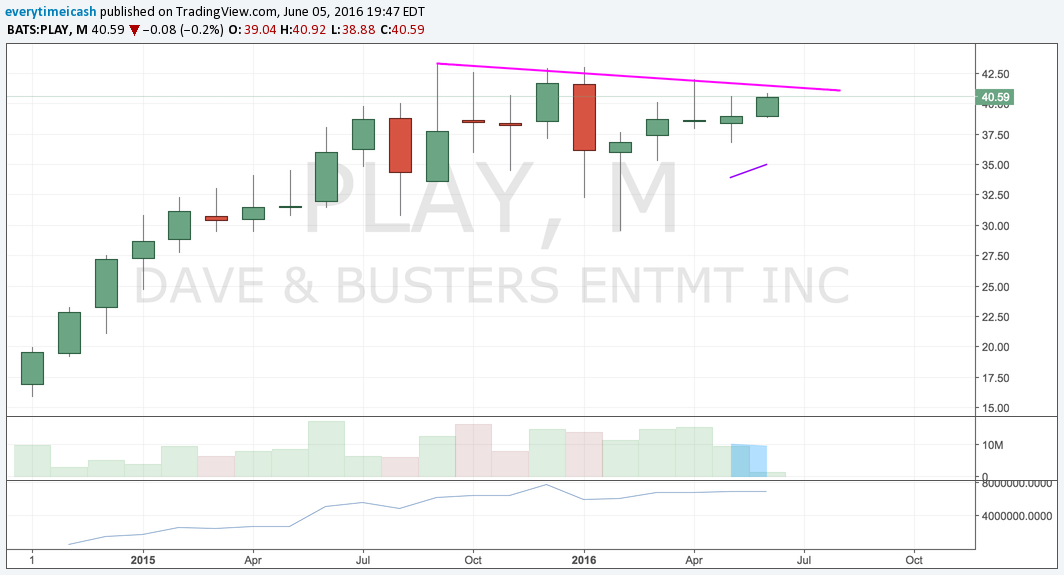

Broke out of multi-month downtrend. Add it to your bullish list. Lowest Macau exposure of all the casinos. 24.35 will lead to further upside.

Clear downtrend about to break on all time frames. Extremely bullish chase if that occurs.

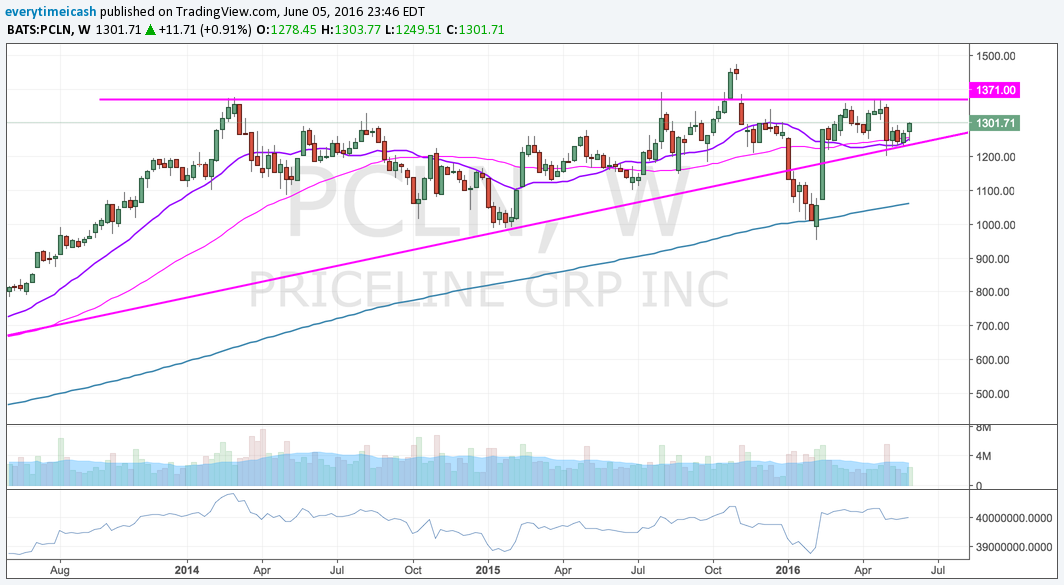

Faked a breakdown and took off. It has been in an uptrend ever since. If this plays like the market has been of late it's poised to fill the gap into the 1317 1331, and 1340 levels and possibly beyond.

One of the strongest names in the strongest group. This had 28 weeks of consolidation. Look for a continued breakout.

Still ready.

The question you ask yourself is: "How much can I risk with a 40% stop out and still fall under/at $100 loss on the day?"

With nearly four weeks of sideways to downside action the pundits would have you think that the market is on the verge of falling apart. The talking heads (for the most part) have you convinced that the sky is falling and that the world economy is abysmal. Hypothetically speaking, even if we are in an outright terrible place in the economy the market doesn't care. Markets unintentionally forecast several months in advance. So with that said, price is truth. Know what you're trading off of and you will be okay. Either direction. I want to be clear and advocate that I am not saying everything is rosey or that they are wrong. I'm simply saying; "Who gives a shit?"

We're not in the business of being "right" we're in the business of making money. Leave the

"being right" to the morons on television who need to fill their ego since they can't fill their bank accounts with their "trading"

After a rest, this name is nearing a breakout and is almost set to resume its trend higher.

Renewed strength with a well defined post-ER range. Keep this one on your list for a potential breakout.

This name has founded a rejuvenation. Currently flagging and poised for higher on a breakout.

Aggressive call buying and at the lower end of is two year range. Strip out the competition bullshit and just look at the price action. A break of 94 sets this for round two.

Here are the levels. Nothing more needs to be said.

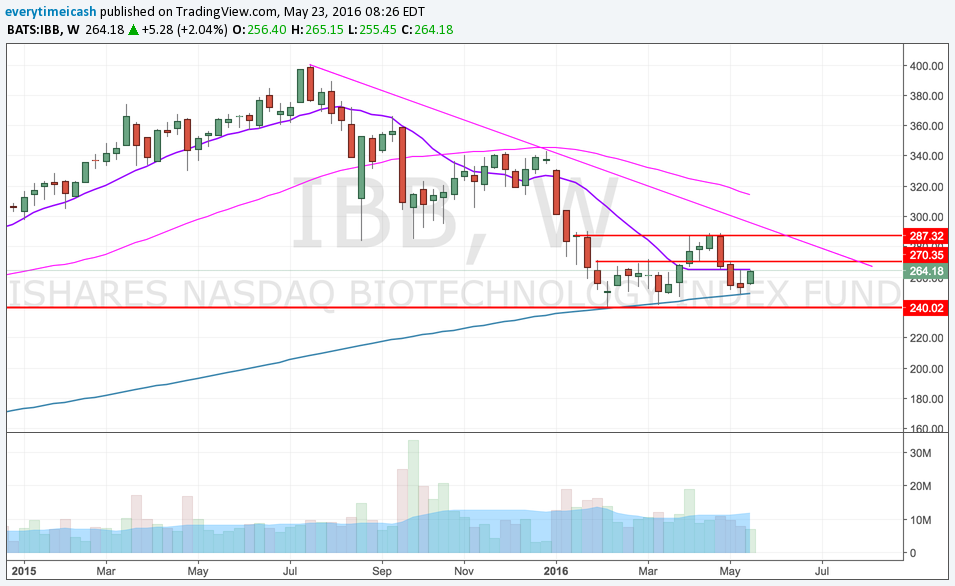

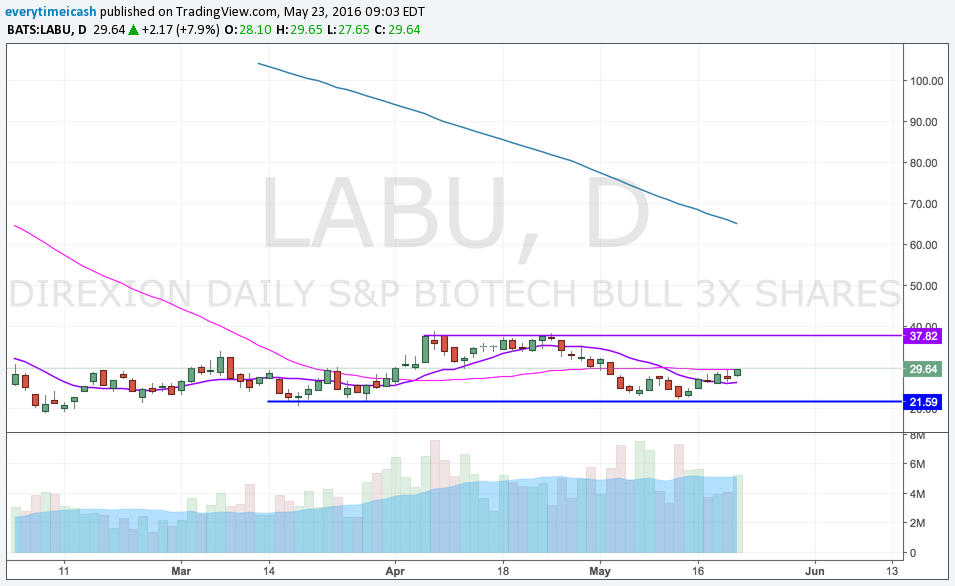

XBI (and in some respect the IBB) has been building a weekly base and is poised for higher highs. The next several weeks will be key in the space as many of these names report vital data that will surely serve as a catalyst.

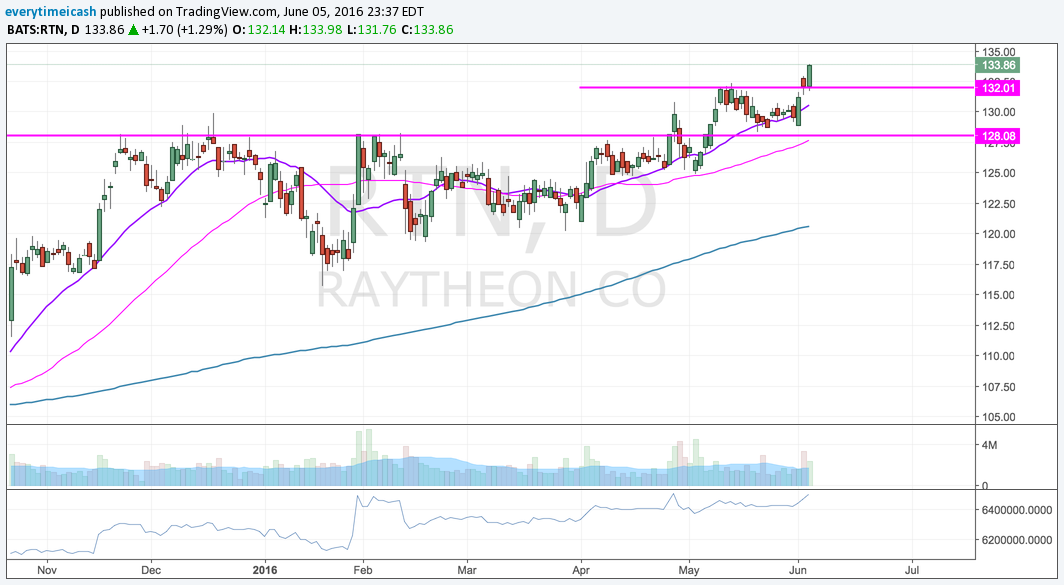

Buffet bottom seems to be the theme here. Look for it to press up to the edge of the gap. Look for the part makers to catch a bid as well.

The retail killer and giant has been basing for round two.

The giant put seller has seemingly put a bottom in this stock. With volume pops in the name, this stock seems poised to break out. Using 14 as a stop this is worth a long. Look for 14.6 as the breakout level.

Multi-month breakout. Look for follow through.

Current Consensus is calling for adj EPS of $1.40 on revenues +6% Y/Y to $13.2 bln.

Q1 Expectations: EPS of $0.37 vs $0.56 year ago on sales -4.3% y/y to $5.96 bln.

Investors are still nervous following the Q4 results which saw the stock sell off sharply after the co posted soft installations Q4 results and Q1 guidance.

The company was unable to address the concerns around an increase in financing costs. They did announce two new refinancing deals this quarter which helped ease tensions.

Consensus stands at a loss of ($0.59) per share on Revenues of $169.55 (which would represent a decline of 31% y/y).

Analyst estimates call for EPS of $0.03, Revs +31.2% y/y to $155.53 mln. Expectations are in-line with the company's provided guidance from their Q4 report for revenues of $154-157 mln.

For RIG, what matters most is the spending of oil explorers and producers. Capital spending for this group has been cut over and over again by many companies since last year, which hurts companies in the drilling and oil service and equipment industries.

For now, oil drillers are aiming to reduce costs to help try and weather the oil slump. But there may be a little relief as the oil rig count, as measured by Baker Hughes (BHI), is expected to bottom in the second quarter.

The most recent weekly oil rig count data, released last Friday, showed that oil rig fell for a sixth consecutive week and are now down at levels not seen since 2009.

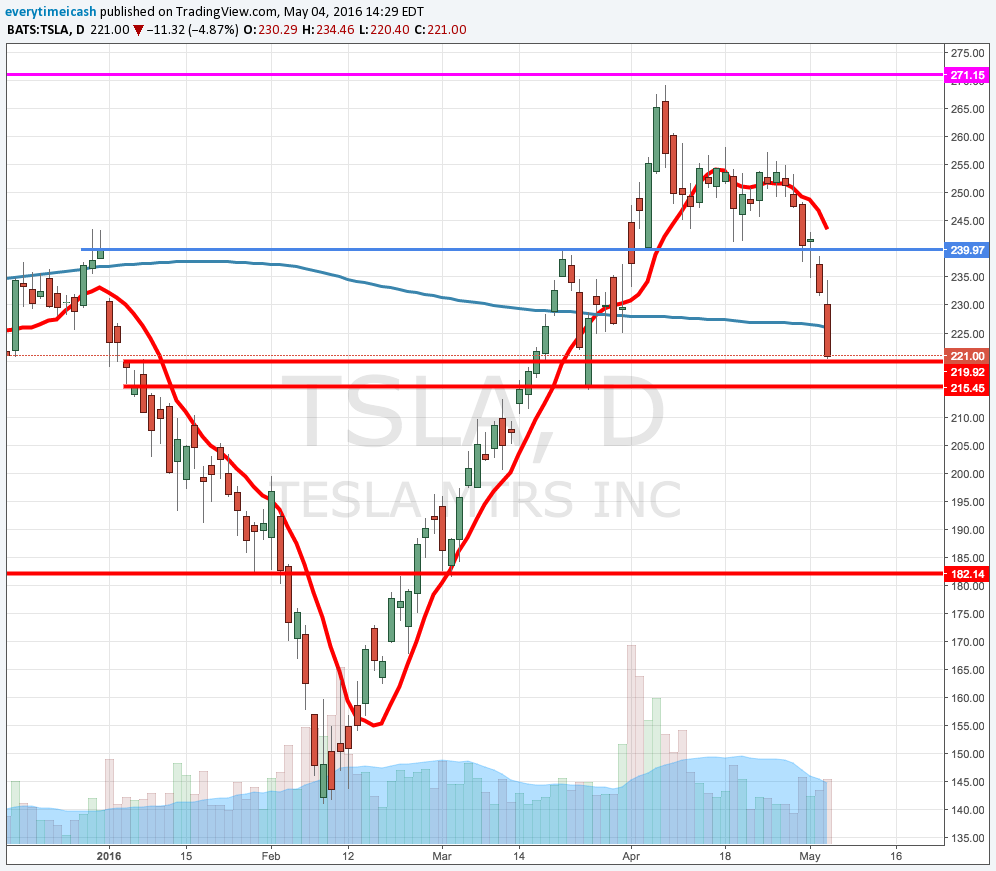

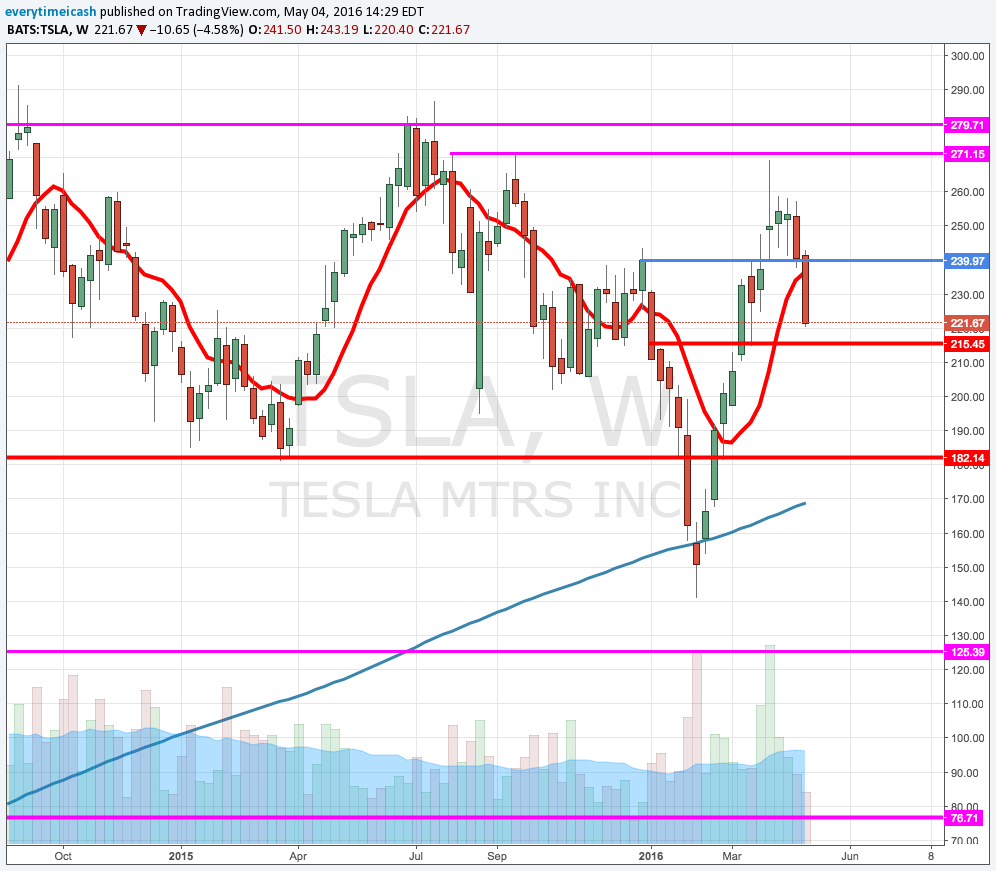

TSLA fell back below the critical 240 level in the market's recent pullback. Shares have come under pressure today following reports that two VPs of manufacturing are leaving the company.

Shares are trading lower by $10.15 at $222.17 in Wednesday's session. The double whammy of hedge fund manager Jim Chanos and high level exiting the company has longs extremely nervous about its Q1 report due out after the close.

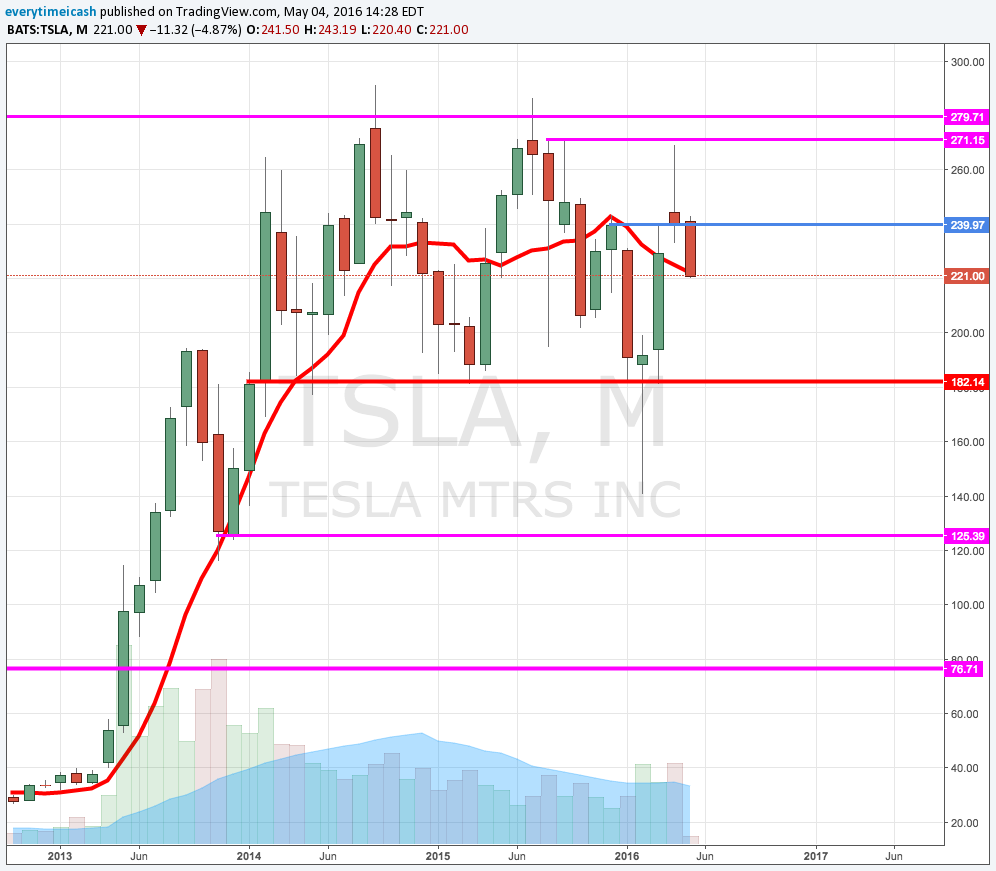

Tesla Motors (TSLA) reported largely in-line Q1 results last night after the company preannounced Q1 deliveries below guidance last month due to Model X production issues. More importantly, Tesla announced very aggressive production targets that seemingly make a capital raise inevitable.

Encouragingly, production has picked up and demand for the Model S accelerated in Q1, with orders up 45% year over year.

Tesla now plans to build 500K vehicles (Model S, X and 3) in 2018, two years earlier than previously planned. Tesla is planning to build 100-200K Model 3s in the second half of 2017. Elon Musk said there is a high probability you will receive your Model 3 in 2018 if you place a reservation right now. Before last night's news, analysts may have assumed a new reservation wouldn't land you a Model 3 until 2019.

As a result, Tesla raised operating expense (to 20-25% growth from +20%) and capital expenditure guidance (~50% from $1.5 billion previously) and backed off its non-GAAP profitability and positive free cash flow targets for 2016.

Both the Bulls and Bears have something to chew on by this news. Bears will say it's an unrealistic product target that will require an excessively dilutive capital raise. But TSLA bulls have faith in their ambitious CEO. Successful execution will put the company even further ahead of the incumbent auto makers in the electric vehicle market and even the tech giants like Apple and Google planning an entrance in the auto market.

Tesla shares are 5% lower today after Elon Musk raised the stakes yet again and signaled an inevitable capital raise.

'Yeah, so the online business, it has been decelerating over the last few years. It's a structural decel, if you look at our Subs business in the aggregate... the trajectory of the online business is it's been pretty linear in terms of the year-on-year growth rate.'

Amazon.com (AMZN) is set to report Q1 earnings today after the close today followed by conference call at 5pm ET.

POT will be releasing its Q1 earnings results tomorrow pre-market with a call tomorrow at 1:00pm ET. Consensus for POT calls for EPS of $0.15 and revs of $1.1 bln. If realized, that would be an EPS decrease of 66% and a revenue decrease of 29% YoY.

A big issue all fertilizer companies have is the recent weakness in farmer cash receipts. This hurts product companies like POT. And, potash prices remain weak driven by both demand and supply issues. Nitrogen prices are struggling as well.

Co expects global potash shipments in the range of 59-62 million tonnes, in line with 2015's total of ~60 million tonnes, but above current demand expectations.

Overall, Potash (POT) doesn't just sell potash. The co sells potash, nitrogen and phosphate. Following is the breakdown of how much each contributes to the co's gross margin.

POT's gross margin exposure by segment: Potash = 56%, Nitrogen = 33%, Phosphate = 11%.

Potash- North America = 34%, Offshore = 66%

Phosphate - North America = 62%, Offshore = 38%

Nitrogen- North America = 87%, Offshore = 13%

Other fertilizer stocks include AGU, BG, CF, UAN, IPI, TNH, MOS, RTK, RNF. POT's closest peers.

Unlike many other companies, expectations for Facebook remain quite high. Failure to meet those expectations could cause a material decline in its stock, which is up 31% over the last 52 weeks.

Ad spending drives Facebook's top line, accounting for 95% of the company's revenue in 2015. FB is a barometer for how advertisers are spending and where they are allocating their advertising budgets.

Facebook has a large international presence with 86% of its 1.59 billion monthly active users at the end of 2015 residing outside the U.S. and Canada and 50% of its total 2015 revenue derived outside the U.S. and Canada. Facebook, then, will have some revealing insight to share on global economic activity and the impact of foreign currency on its operating results.

FB announced that the board of directors has approved a proposal to amend and restate existing certificate of incorporation to create a new class of non-voting capital stock, known as the Class C capital stock.

If approved, it will issue two shares of Class C capital stock as a one-time stock dividend in respect of each outstanding share of our Class A and Class B common stock. This proposal is designed to create a capital structure that will encourage Mr. Zuckerberg to remain in an active leadership role at Facebook.

“The adoption of the proposal is subject to the approval of our stockholders at our 2016 Annual Meeting of Stockholders to be held on June 20, 2016.”

FB breaks through all time high on stellar report, again.