Current consensus stands at EPS of $0.10 on Revenues of $607 mln.

Wolf's Den

Current consensus stands at EPS of $0.10 on Revenues of $607 mln.

Shares of EBAY were blasted following the Q4 report. EBAY managed to report an in line quarter, but downside guidance to both Q1 and FY16 led to selling pressure that would drop the stock 13%. EBAY shares were able to settle at the $22 level in mid-February and have been able to climb back toward $25 ahead of tonight's report.

An attractive valuation has been the primary driver for the move back through the post-earnings gap down. An attractive valuation is all that's saving the stock right now.

Consensus calls for EPS of $2.00 (versus $2.33 last year) on revenue of $51.98 bln (-11.6% YoY).

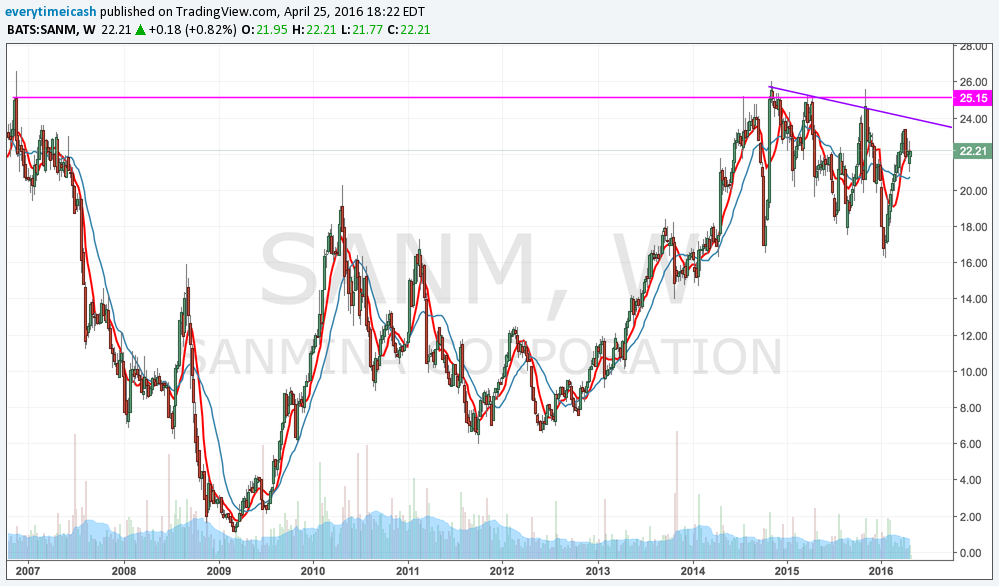

SANM is coming off a solid Q1 report. Its EPS were in line and its revenues actually missed expectations, but the revenue miss was expected. However, SANM operating margin was higher than expected and its Q2 guidance was also above consensus. The stock jumped 8% in reaction and has been a steady performer since as it would rally through a slew of key moving averages to push to $23.50.

Shares were ~30% higher from when it reported Q1 results. The stock has retraced back to its 50MA ahead of tonight's report. The decline is most likely some profit taking after a strong run during the quarter. The stock is sitting on its 50MA ($21.80) and has key support in the $21 zone.

Key Metrics

Q2 Guidance

Q1 Recap

SANM reported Q1 (Dec) earnings of $0.58 per share, excluding non-recurring items, in-line with the Consensus of $0.58. Revenues fell 9.9% year/year to $1.53 bln vs the $1.59 bln Capital IQ Consensus.

Apple's revenue guidance for the period implies it will post its first year-over-year decline in quarterly revenue since 2003

With poor earnings from $V $SBUX $GOOGL/$GOOG and $MSFT, the market had every reason to let the bottom fall out and collapse on Friday. Though we started lower, we ended the day slightly in the positive for the S&P 500. The Q's took it early but finished moderately lower. The A/D line continues to broaden and the market continues to catch a bid. Unlike the last couple of years, the broader market participation has been stellar and it seems every couple of weeks there is a rotation into a new group. The main focal point on Friday was the IWM which ended firmly in the green. Until this musical chairs of money rotation ends, there is no reason to believe that the bears have any semblance of control. There are two levels of support currently where dip buyers step in. Near the 9 and the 20MA's. It's important that the momentum continues and the market continues to churn higher as we've broken our downtrends (for now).

Entire sector is seeing strength and is reversing its downtrend.

Flagging at its downtrend line and at resistance.

Broke monthly downtrend and breaking into resistance.

TSLA Flagging into support. 20D better hold.

Bull Flag, multi-day consolidation.

Flagging and ready to break out.

Ready to rip

All bio ETF's are ready to rip and some have started to move.

Basing for a breakout.

Basing for a breakout

"Poor" earnings results but found support and bounced.

Breakout looming

Visa beats by $0.02, reports revs in-line; lowers rev guidance, EPS growth guidance.

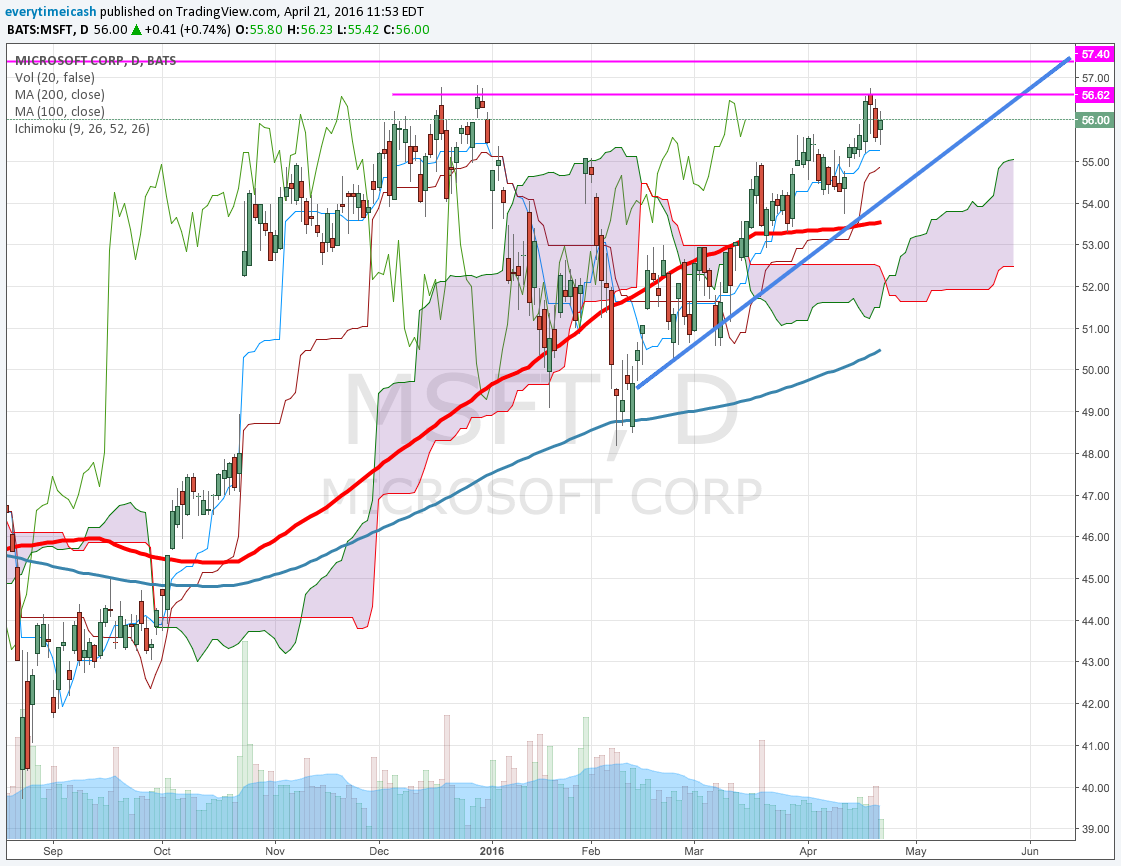

Microsoft is set to report Q3 earnings after the bell. The company releases their earnings results on their website. In addition, there is a conference call scheduled at 5:30pm ET, where management will provide Q4 revenue guidance.

There is no other competitor in the cloud space other than AMZN really. MSFT strategy focused on being that second competitor since they realize they could not overtake the 800lb gorilla in the room known as AWS.

Dynamics products and cloud services revenue grew 9% in constant currency with Dynamics CRM Online seat adds more than doubling year-over-year.

Xbox Live monthly active users grew 26% year-over-year to 46 million.

No matter how you slice it, this wasn't a good quarter for MSFT. As discussed in the trade packet, MSFT was a no touch as it was going into a report with lofty expectations, high IV, and into 20 year overhead supply (charts below). As expected, it traded back to the 100 day.

Alphabet (GOOG, GOOGL) is set to report Q1 results tonight after the close with a conference call to follow at 4:30pm ET. GOOG reported Q4 results at 4:01pm.

GOOGL reported Q4 (Dec) earnings of $8.67 per share, $0.58 better than the Capital IQ Consensus of $8.09. Revenues rose 18.5% year/year to $21.33 bln vs the $20.76 bln Capital IQ Consensus.

Revenue Segments

It looks like expectations are growing as margins are contracting. This is not a good scenario for a growth company. The longer this goes the more likely the old google days are over.

Some of the most exciting news in this space in the past year was when Halliburton (HAL) announced an agreement which HAL will acquire all the outstanding shares of Baker Hughes (BHI) in a stock and cash transaction.

In their last report, Halliburton said, "We are enthusiastic about and fully committed to closing the compelling BHI transaction, and remain confident we can achieve annual cost synergies of nearly $2 billion." BHI is the world's third largest oilfield services company. SLB is the largest and HAL is the second largest.

Technicals

Technically, BHI remains in context of its downtrend off the 2015 highs, below its down-sloping 200-day moving averages (48/49). Energy as a whole has stabilized during Q1 of this year as Crude rallied back towards four month highs off the Feb lows.

BHI currenty sits along the top of its own 4-month range highs near the $47-area. A positive response to earnings will need to clear this resistance as well as the 200-day ma's above near 48/49. This would ignore more short covering. A negative response to earnings will liekly cause a test support near the 50-day ma's at 43/44, followed by its YTD range lows near 38/40.

In their annual report, Halliburton stated that the Baker Hughes acquisition may not be accretive, and may be dilutive, to their earnings per share in the near term.

A Technical Perspective

Technically, HAL has been on the mend off its January/February lows with a gain of more than 40%. It's recent upward momentum is clearing its longer-term downtrend line with price challenging resistance at the 40/41 area from the latter half of 2015. Expect price to push higher towards 45 on a positive response to earnings. A negative response will likely knock price back down towards the 36/37 followed by 34.

Options Activity

Based on HAL options, the current implied volatility stands at ~ 30%, which is 2% lower than historical volatility (over the past 30 days). Based on the HAL weekly Apr22 straddle, the options market is currently pricing in a move of ~2% in either direction by weekly expiration (Fri).

OIH WILL BE IMPACTED BY THE REPORTS

Capital IQ EPS consensus: 1.16 Capital IQ Rev consensus: 5.82 bln

Reports Q1 (Mar) earnings of $0.34 per share, excluding non-recurring items, $0.15 better than the Capital IQ Consensus of $0.19; revenues rose 3.0% year/year to $2.03 bln vs the $1.87 bln Capital IQ Consensus.

Attributable production totaled 1.23 million ounces, compared to 1.19 million ounces in the first quarter of 2015. During the quarter, higher production at Batu Hijau and Kalgoorlie and inclusion of CC&V more than offset declining production at Yanacocha and the sale of Waihi. Attributable copper production totaled 38,000 tonnes compared to 37,000 tonnes in the year ago period as Batu Hijau continued to mine higher grade ore.

Attributable gold production is expected to increase from between 4.8 and 5.3 million ounces in 2016 to between 5.2 and 5.7 million ounces in 2017, and remain stable at between 4.5 and 5.0 million ounces through 2020.

Attributable copper production is expected to be between 120,000 and 160,000 tonnes in 2016 and 2017 before decreasing to between 70,000 and 110,000 tonnes by 2018. The decline is due to the depletion of higher grade Phase 6 ore at Batu Hijau in 2018. Production at Phoenix Copper Leach and Boddington is expected to remain stable for the period.

WYNN Takes a hit after hours with the miss.

Coca-Cola (KO) is scheduled to report Q1 earnings tomorrow, before the opening bell, at 6:55 ET.

Current Consensus is for FY 16 EPS $1.95 on revs of $42.3 bln

Last quarter, KO beat EPS by $0.01/share w/ revs in-line.

The stock price has been in a steady uptrend since, rallying bounce on the 50 day 3 times during the last quarter. The stock is currently up ~9% on the quarter and is near its 50 day.

YHOO pricing a 8.3% move on 25,300 contracts traded. Calls outpace Puts 2/1 with IV at 39.3% and 171% higher than their historical (30 day) average.

Based on INTC options, implied volatility stands at ~ 25%, which is 57% higher than historical volatility (over the past 30 days). Based on the INTC Weekly Apr22 $31.50 straddle, the options market is currently pricing in a move of ~4% in either direction by weekly expiration (Friday).

GS reported Q4 (Dec) earnings of $4.68 per share compared to the Consensus of $3.62; revenues fell 5.5% year/year to $7.27 bln vs the $7.04 bln Consensus.

Netflix ($NFLX) is set to report Q1 results tonight after the close with consensus at EPS of $0.03 on Revenue of $1.965 bln.