Q4 Recap: IBM beat on Q4 non-GAAP EPS of $4.84 vs the $4.81 Capital IQ Consensus and reported revenues in-line at $22.06 bln.

Wolf's Den

Q4 Recap: IBM beat on Q4 non-GAAP EPS of $4.84 vs the $4.81 Capital IQ Consensus and reported revenues in-line at $22.06 bln.

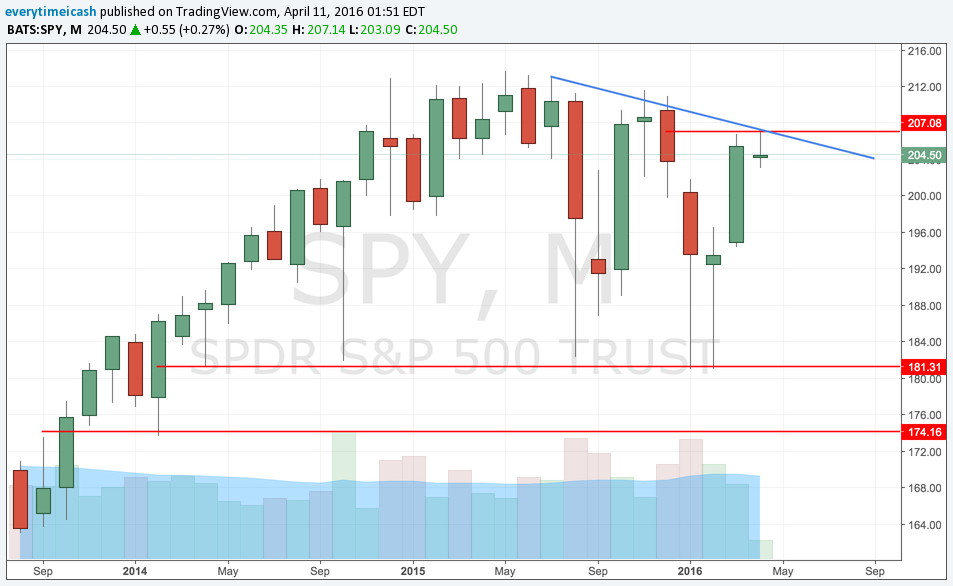

Against "all odds" the SPY rallied back into its downtrend that it started back in 2014. As you can see in the charts, SPY has resistance on all time frames here. It is not bearish however and has support sitting at 207, 206, and the 20. "Line int he sand" remains 2025-2030ish. Recently, selling into strength has been the play. With earnings season around the corner, it is important not to overtrade and blow your wad before getting a chance to play the moves that will potentially yield better results.

With DOHA being the headline of the weekend, and with oil "tanking" at the moment, it will be the caution that you will hear about from all the pundits. Bias remains that the market is healthier underneath than it has been in quite some time and it's important to not trade the headlines and only focus on the price action. If you are confused sit back and wait. No need to trade in the slop.

This has been one of the strongest components in the market as of late. Many of the issues here have been at/near highs. Many of these issues are going into resistance and "should" pause.

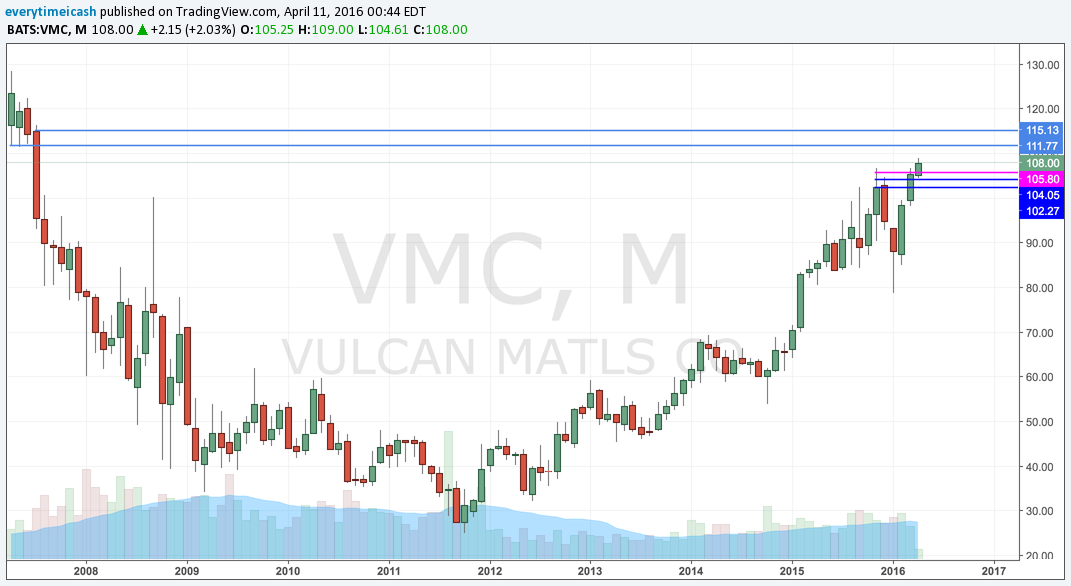

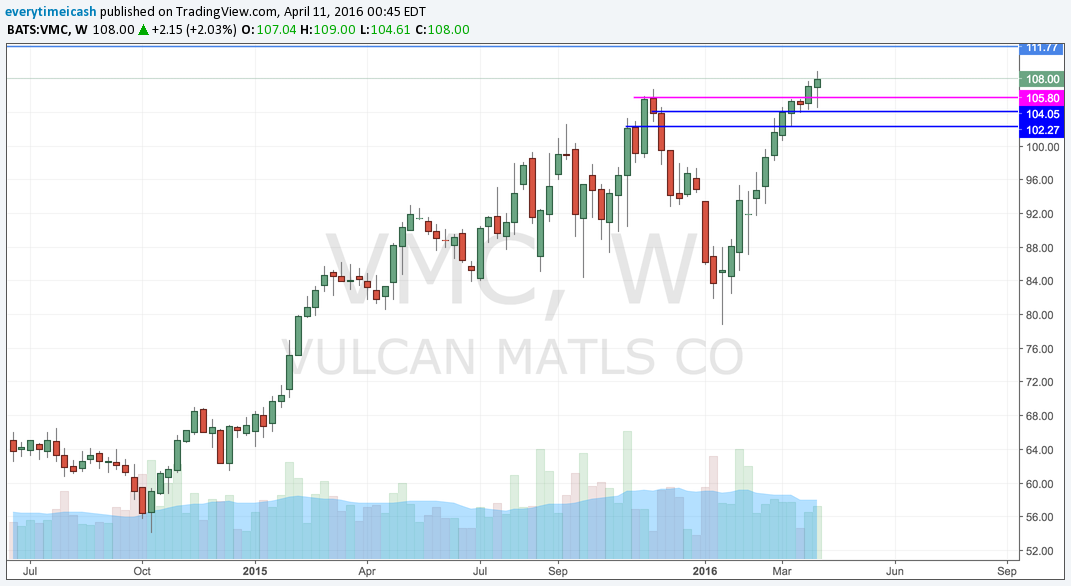

Resistance on the monthly and broke out on the other two time frames. The larger time frames are the ones that matter more.

MMM into resistance.

Into downtrend resistance.

Into downtrend

Earnings this week, will be interesting to see what they report/say.

Rounding bottom and broke out last week. Above 17.5 gets it going another 13%.

80 Trigger to be "safe"

ADBE broke out on the daily but has not yet on the weekly.

FCX approaching a range breakout.

Money flow went into a chase for yield. Now we've got a potential H&S and we're facing resistance.

People continue to bet against this name (foolishly). It has been consolidating and getting tighter. Levels above.

CPS

Nearing a weekly breakout.

As expected, last week showed us a range bound week (inside week) following a 12% run up in the SPY. Action was quite volatile relative to the last few weeks with a couple of false breakouts and breakdowns.

The SPY was range bound last week with 20 and 200MA functioning as support. As highlighted last week the 2030 level has functioned as support for the SPX and 2070 has been resistance. After last week's inside week we're going to pause for a break to the upside above 2070 or a breakdown below 2025. My bias is that a new wave of leadership is forming in the markets and that this rally in gold can propel for a while longer. That said, the SPX/SPY is in a downtrend since May of 2015 with lower highs. We will in fact see as earnings season kicks into high gear and the banks start to report.

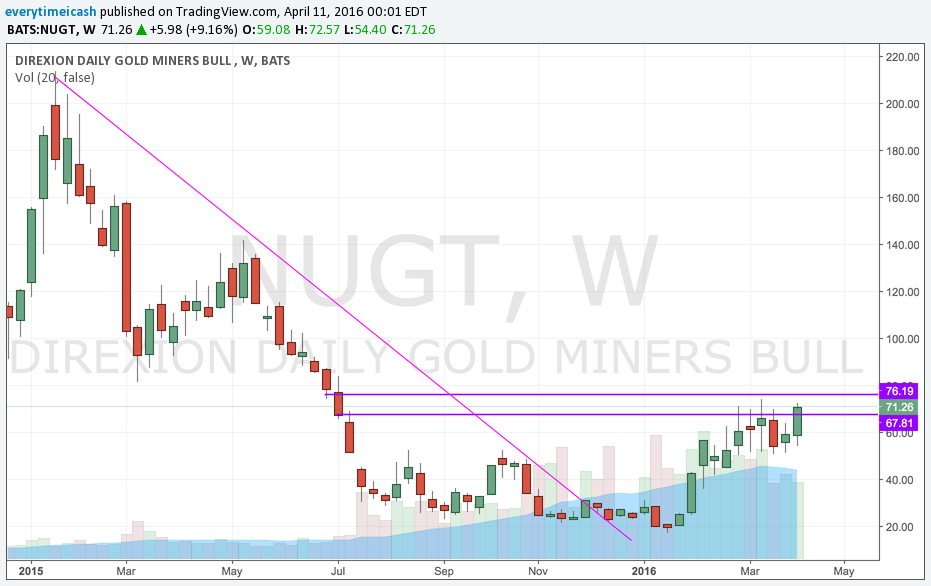

As seen recently, gold has begun to break out as it broke its downtrend with a higher high and channel break. After a period of consolidation, it is apparent gold is ready to make its run again. As gold goes, so do its derivatives

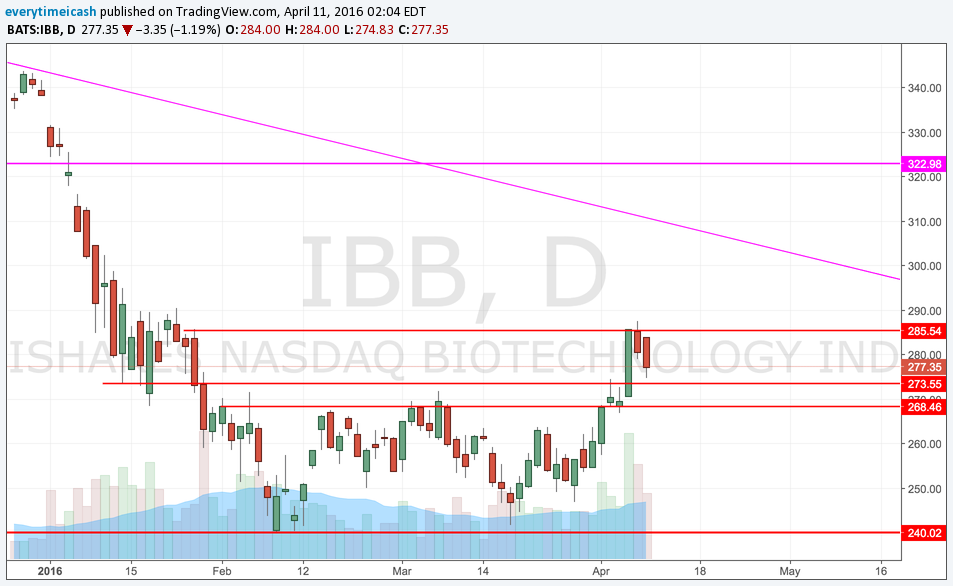

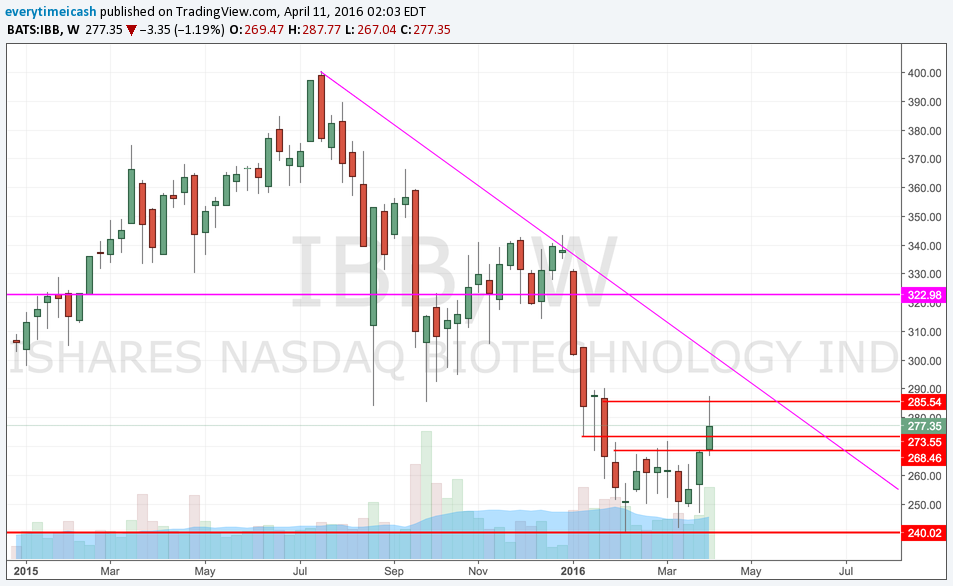

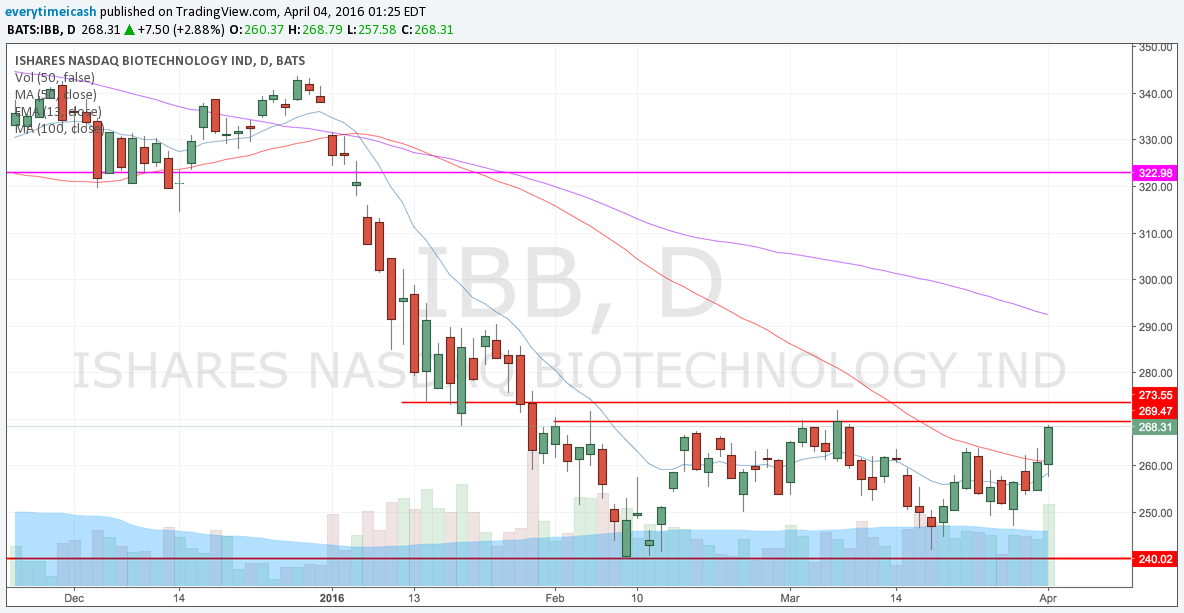

As noted two weeks ago, the IBB bounced of its 50% retrace from the highs and has continued the run since. Our target of 285 was reached and we're now waiting for some consolidation before a potential run higher. A potential retrace to the downtrend is what we're potentially looking for.

Aggressive call buying into consolidation and this one is set to take off higher.

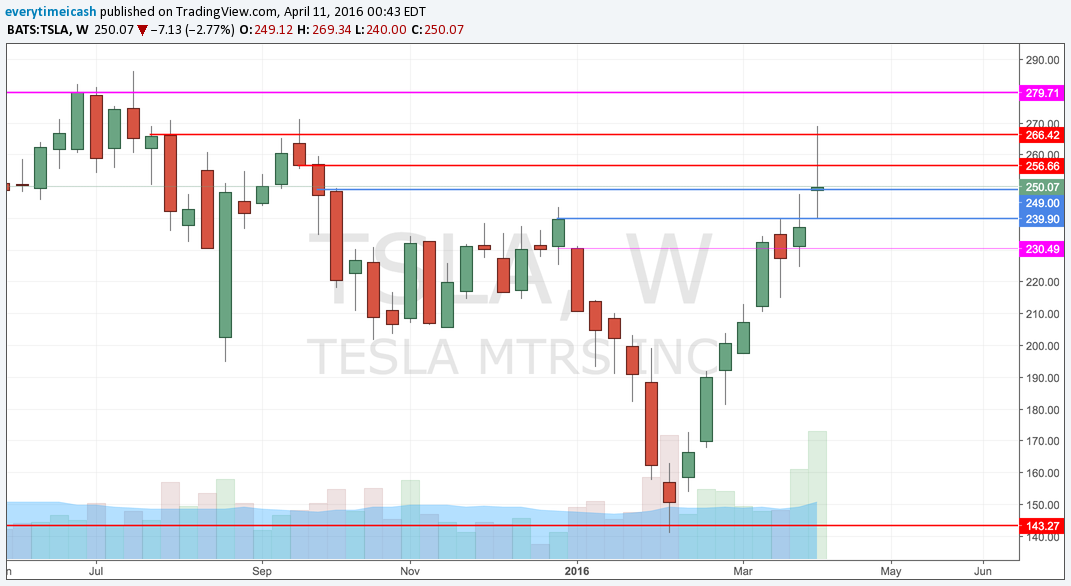

After a torrid run up almost doubling its share price in approximately six weeks, TSLA finally hit resistance and started to turn lower.

After a face rip week, last week saw some consolidation. We're working with a flat 200MA and a breakout above 604 to spark this thing.

After leading us on the way up, XRT has started to roll over as it hit resistance into its previous up trend.

Both in a flag and looking to break up or down. (Bias Up)

Ignore the "Fast Money" stupidity by the guy who has a 17% stop. Stick with trend until it's broken. Currently 97.5 has functioned as support and below that is the box breakout support of 96. Last week we saw some continued May C buying by the wise guys.

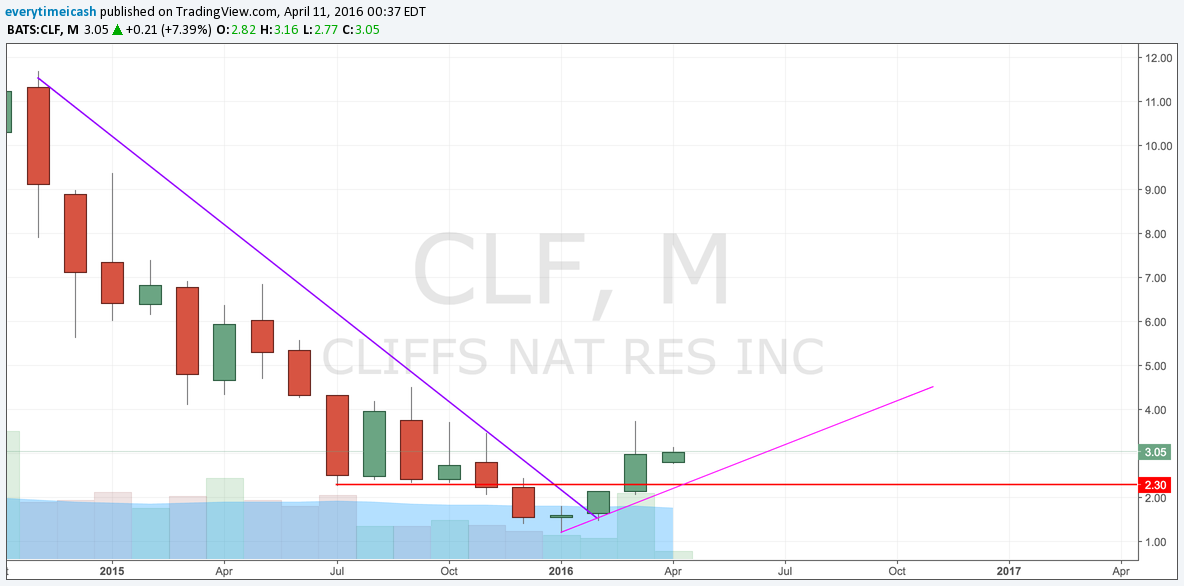

My favorite materials company out there. Period.

Some China names have recently caught a bid and my favorite setup at the moment is potentially BITA.

This is a former high flyer with recent accumulation volume.

This showed a break in 2014 and has been in a downtrend since. As of late however, it has showed some signs of stabilization in an attempt to get back to its down trend.

Basing for a potential break to the downtrend.

With 35% short interest, zero debt, 45% YoY growth, decoupling from GPRO chart, base building on multiple time frames, and a large institutional ownership group AMBA is a buy.

The SPY continues to show resilience and defy the bearish thesis that has plagued those who have missed out on this recent rally for over a month and a half now. Last week SPY found support yet again off the 8/9EMA and thrusted upward to crete a new high on the year. As of now, "the trend is your friend." That trend remains upward for now as we've erased all our current year losses and the underlying market internals appear to represent a broader based rally.

Common upward themes remain as dip buyers step in at every sign of weakness and continue to press the pain upwards. Until this dip buying and the internals start to roll over the trend remains upward. Ignore the Dan Nathans and Brian Kellys of the world that continue to spew nonsensical caution.

SPY broke out above resistance after consolidation. The above red line will function as resistance and the blue line is a downtrend the SPY formed starting August.

Market has found a continuous bid by finding itself in a money rotation cycle from one sector to the next. It started with a short cover rally in energy and materials and has continued from sector to sector. Most recently, (last week) biotech and the FANGs found an underlying bid after several days of consolidation. 2030 SPX support will be our near term line in the sand.

GWPH has consolidated since it gapped higher and has held 70 support. Look for a breakout above the near term (purple) trend line and the larger (blue) line for a larger move.

Kate has been my largest swing position for weeks now and this is now "my main bitch." We're looking for a breakout above the resistance line as it has seemingly found dip buyers at every turn. The 13MA has been support.

KATE broke out above recent resistance. We have a convergence of trend line and a "cross up" forming.

AMZN Showing continued resilience on both the daily and weekly time frames. On the daily it is finding resistance against a flat 100MA. A breakout above gives first a target of 610 and then clear skies above to 630ish.

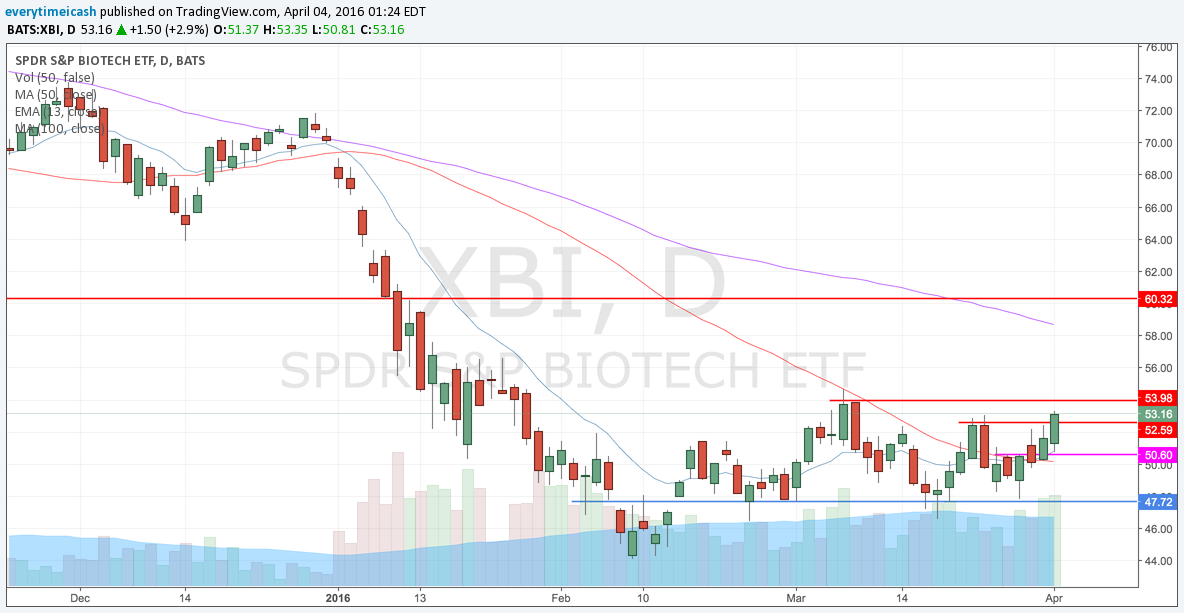

Bios have been basing for quite some time now and showing signs of a bottoming formation. XBI poked its head out above initial resistance last week with sharp Call buying. IBB followed shortly thereafter.

Look for a continuation to 284 on IBB and 57-58 on XBI.

AMBA pressed up against a downtrend that's still in tact. A break above the downtrend and this one will have legs.

DG Breaks out of consolidation to all time high

All time high breakout after long consolidation.

NDAQ nearing a breaktout

TSLA Failed but held previous "support"

TSLA has been on a major tear and failed after the announcements Thursday night and Friday morning. Looking for consolidation. A breakout above 250 likely sends us for a 266 test. 275 looks like the trigger on the monthly.

SQ broke out of its IPO base last week and then quickly retreated back to the breakout point. Here are the trends.

“Successful trading is always an emotional battle for the speculator, not an intelligent battle...A man must know himself thoroughly if he is going to make a good job out of trading.”

IF you've ever taken a statistics course you have certainly heard the term "Regression to the Mean" (RTM). If you were drunk and/or tired in class, or simply never took a stats class and don't know what I'm talking about let me give you a quick definition.

Let's see what that shit looks like:

Regression to the Mean (RTM)

Looking at the picture above you get a clear demonstrated example of how RTM works. Sometimes things deviate to the mean to the upside and sometimes down. However, they seem to travel along a defined trend line. Applied, you can make this case for every stock that has ever traded in the history of stocks.

Understanding this phenomenon will help you infinitely with your trading ability. If you apply this theory to your trading you will see that it consistently holds true. Every individual has an average trading baseline that he/she trades along. Sometimes the curve goes in your favor, sometimes it does not. If you've developed a system however, you will find that over the course of the long run you will revert back to your average baseline.

Do you feel like you're on a hot streak? Slap yourself. You're not. I know, I sound like a douche saying that. It's true though. It also works the opposite ways. Sometimes we fall into "hot patches" where we basically can't miss in the stock market. Sometimes the opposite happens. Thats why it's very important to remain level headed when you trade. You must maintain the poise necessary to move forward regardless of momentary outcome.

There will be hot streaks and there will be cold ones. In order to maintain success in this business you've got to learn to temper your expectations and stick to your rules. Don't adapt the rules for the circumstance. If something's not working, evaluate whether or not you're adhering to your rules. Don't look for the change in them. Look internally and realize whether or not you are actually holding yourself to that standard.

If you can learn anything from the definition or the write up above its simply that the more you try the more likely you are to bring down your average. Like a basketball player, the more shots you take the more likely it is you will not be perfect. So one of two things should be done:

The market typically chops 70% of the time and gives direction 20-30% of the time. So in theory you have a couple of choices, outperform the market 70%+ of the time or mostly trade during the times in which the market is trending.

Mathematically it works like this:

If you only traded 30% of the time and had an overall outcome of a +24% account value (this example assumes you're trading options) during those times you would compound a $3000.00 to over $58,000 in less than a year.

The above assumes that you are disciplined to not trade while the market is chopping around and assumes that you are equipped to know when the markets don't chop. Obviously the results won't be linear but the example is to show you a simple proof of concept;

For fun I want to show you the power of compounding and keeping your risk small. Below is an example of how fast you can compound an account over the course of 50 years with no additional contributions.

1 : 3380.47

2 : 3809.2

3 : 4292.3

4 : 4836.67

5 : 5450.09

6 : 6141.29

7 : 6920.16

8 : 7797.81

9 : 8786.77

10 : 9901.16

11 : 11156.87

12 : 12571.84

13 : 14166.27

14 : 15962.9

15 : 17987.4

16 : 20268.65

17 : 22839.23

18 : 25735.81

19 : 28999.76

20 : 32677.66

21 : 36822

22 : 41491.95

23 : 46754.17

24 : 52683.77

25 : 59365.39

26 : 66894.41

27 : 75378.3

28 : 84938.15

29 : 95710.44

30 : 107848.92

31 : 121526.86

32 : 136939.51

33 : 154306.87

34 : 173876.84

35 : 195928.78

36 : 220777.45

37 : 248777.56

38 : 280328.78

39 : 315881.49

40 : 355943.17

41 : 401085.67

42 : 451953.38

43 : 509272.38

44 : 573860.86

45 : 646640.79

46 : 728651.02

47 : 821062.21

48 : 925193.45

49 : 1042531.14

50 : 1174750.19

“Success in investing doesn’t correlate with I.Q. once you’re above the level of 25. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

I am certain that many of you who have come across my online profile have come to the belief that I am/was full of shit at one point or another. If you haven't I admire your naiveté and thank you for your trust. Though I've encountered what most would quantify/qualify as "success" when it comes to trading and though I've been fortunate to never come on the negative end of the stick, this does not mean that I've never faced pitfalls. This also doesn't mean that I haven't faced my own level of disappointment and frustration. Most importantly, it doesn't mean, and for lack of a better term, the market hasn't made me her bitch from time to time.

The longer you stay at the trading game, the more you will be humbled. I liken the market to a game. You start at a particular level in this game. Some have a cheat code (more capital) some have to begin at the very beginning with very limited resources. Fortunately however, whether you're insanely wealthy or only have a couple hundred dollars to your name there are always opportunities.

Personally, I've been on both sides of the equation. I've seen a $200 trade blossom into $21,000+ in a matter of an hour. I've also had the misfortune of watching $9,000 evaporate into thin air on a bogus rumor. Both feelings, though unique on their own, are rooted one in the same. Euphoria and anger both different sides of the same coin. I'm going to share the most valuable lesson I've ever experienced as a trader; even though I didn't know it at the time.

I'm not sure why you trade but I'm almost certain for most of you it's to earn income/make money. At least that's why I got back into trading. The ironic part is in order to make money, you gotta learn how to lose it. Sounds "bass aackwards" i know, but it's not. What I mean is you've gotta learn how to trade good setups. Setups that work in your favor. You've got to learn to know when to say "I quit" and tap out of these setups too. Without a plan or without defining a trade you'll simply compound your losses and wind up worse off than you were.

Like I said above, I've been lucky to stay ahead of the 8 ball during my career. But I've faced my fair share of set backs.

In late 2013 I discovered the power of leveraging weekly options into a trending stock. Previously I'd only traded commons or monthly options. Initially, I discovered this power with three very volatile stocks -- FEYE TWTR & TSLA.

More specifically, I was able to capitalize on riding TWTR for every one of its breakouts to fresh highs and compound my account quite rapidly. "Feeling like I was on a hot streak" I started to push my luck with TSLA. I attempted to replicate my process with TWTR in TSLA as it made a new high seemingly every single day. I continued to take on risk and leverage my positions for further upside gains. I was aggressive and continued to press my luck.

In early January 2014 I learned the most important lesson of my trading career. Don't fight the trend, and never average down a weekly losing position. As you can see from the chart below (one I've shared on multiple occasion) I learned (though didn't know that at the time) the hard way, that averaging down on losing positions will destroy you.

What that above chart doesn't express numerically is that I was able to 7x my account from the start of November simply by staying with the breakout trend and backing off when it failed. On the week of January 9th, while "expecting" TSLA to break out and continue higher after a "brief pause" I made the bullshit move of "averaging down my cost" thinking that I wouldn't need much of a move to get me going. What I failed to realize was that TSLA stalled against a major trend line and at a gap resistance and it subsequently was going to back test its previous breakout level. I was stubborn and it cost me. That mistake erased over a month and a half's worth of work, patience, and more importantly, gains.

Cognitive tunneling is a phenomenon in which a a psychological lack of attention takes hold without obstructing your individual vision. This phenomenon occurs and is defined as an event in which an individual can't see what's in front of them because of an unexpected circumstance. Specific examples of this occurs when people are so focused on one particular action that they fail to see the greater picture and subsequently cause damage to themselves as a result.

This effect is just how dangerous the markets can get. Sometimes, we get so fixated on a particular instance or result that we fail to see what's going on around us. In the above example, I was so concerned with my own personal position in TSLA that I neglected to see the bigger picture; TSLA rejected the gap and was failing. Though the following week was a tough one (especially since the following week TSLA broke above the previous failed breakout level and continued on to make new highs) it was a pivotal one in my trading career.

It was a stern reminder to never average down a losing position and to set a stop and respect it. It was also a reminder that I/we are never smarter than the overall group. That momentary pain, though brutal, turned out to be the most important lesson that I've ever learned.

The most important lesson I received the week of Jan 9th was that capital preservation is the key to success in the market. Leverage only what you're willing to lose, and stay humble with the idea that you may in fact be wrong. Doing so will only allow you an opportunity to add another life to your trading career.

“I had made a mistake. But where? I was bearish in a bear market. That was wise. I had sold stock short. That was proper. I had sold them too soon. That was costly. My position was right but my play was wrong.”

As I write this, the markets have swung from 201 to 197.5ish back to 199 in the SPY. The swings have been wild and back and forth. Bulls will argue that the economy isn't as bad as people are making it out to be and central bankers are on your side (Super Mario). Bears will argue that we've come too far too fast and we're setting up for a violent failure, market breadth is dampened, and leaders/momentum is rolling over.

Well, and I mean this without it being a cop out, both parties are correct in their assessments. We're in a position now in the markets where our accustomed leadership is waining (think #FANG) and the bears have seemingly lost control in the last several weeks. This sets up for one of two possible scenarios;

Well, technically there are three scenarios. But the third scenario is one that will yield back to the first two;

For people like us, this means we're left with limited options. The times of buy and hold are likely over -- at least until further notice. We've got a flat 100MA, 50WK MA 100Wk MA and 200DMA overhead. A literal tug of war between the bear and bull camps. Positions that have been on for years are starting to unwind (#FANG distributed and short covering in depressed energy assets). The moves are subsequently violent as those who look to get out are getting out and those who are finding "value" are getting in for "the next leg" whatever that means.

As we see above, the SPY longer term monthly trend remained in tact with its most recent test of 1800. This case emboldens the bulls to make the argument that we are still in trend and we have corrected. Furthermore if you look below, you'll see a chart of previous bull market bursts and their respective PE ratios at the peak. In this market we have been trading between 16-18x for quite some time now and the overwhelming euphoric conditions have simply not been there.

SPY PE Expansion in Bull Markets

Markets like this are designed for those who are "professional" in demeanor and nature. Point your attention to the figure below to understand how markets like these (when/if healthy) will and do work.

As you can see from the figure above markets suck in both buyers and sellers at max pain points

Though the above illustrates a bullish outcome, the reverse is also very true. In many cases issues resolve to the downside. When that happens, market declines typically precipitate and escalate more violently than the upswings. With the bull market top currently closer than the recent lows, it's difficult from a risk reward perspective to buy the top expecting higher. Thus is the bear case. In addition, economic outlooks don't give an optimistic view.

Again if you refer to the above charts, we have lots of overhead supply, MA's rolling over on larger time frames, and overall markets decelerating. Lack of breadth and leadership continues to be the theme and the previous outperformers are not participating.

Canadian Solar (CSIQ) is set to report Q4 earnings tomorrow before the market opens with a conference call to follow at 8am ET.

CSIQ is considered to be one of the top Chinese solar players in the market. CSIQ has been a volatile name in the past and has seen aggressive selling in reaction to its last two earnings report. A positive pre-announcement on February 16 "should" take some of the earnings reaction out of play.

February 26 Pre-announcement

Previous Reactions

Q3 Recap

The stock is in the midst of a recent rejection of its 200 sma (currently $23.45) on March 3. It is attempting to stabilize at its 50-sma ($21.45) ahead of its report. CSIQ promises to be one of the more volatile names tomorrow.

Downside FY 15 comps guidance of +2.5-2.8% vs prior guidance of +3-3.5%

Downside FY 15 revs guidance of +8% ($19.5 bln) vs prior guidance of +8-9%

Guidance to Look For

On March 1, DG's closest peer Dollar Tree (DLTR) reported earnings that missed EPS, revs, and guided FY17 EPS below consensus. DLTR opened trading slightly down and fell as much as ~3.5%. DLTR eventually closed trading up ~2% at $82.03, the strength of the broader market could've helped the surge. The stock has sold off ~7% since 3/1. DG did spike lower on the DLTR report, but the dip was bought and the stock has been consolidating into earnings.

On February 23, Buckingham Research initiated w/ a Buy; tgt $94

On February 16, Morgan Stanley upgraded to Overweight.

Currently, $DG is consolidating just beneath recent multi-month highs. $76 is the current resistance, and the 50 day MA is $72.

Comparing that to last year's stats around the same time, URBN had an EPS of $0.60 and $1.01 billion in revenue. In 2016, the stock is up nearly 22% and shares of URBN are trading at $27.99/share.

Currently, the retailer is worth about $3.2 billion and has a massive growth trajectory worth investing in. The firm has a $30 price objective and buy rating from Bank of America’s Merrill Lynch due to its unique private third-party apparel selections. If its stock gets cheaper, private companies would be heavily interested in owning Urban Outfitters.

Urban Outfitters has managed to shrink its float nearly 20% by buying its stock on and off for the past four years and accumulated its total earnings.

On January 7, co reported Nov/Dec net sales were flat y/y

Comparable Retail segment net sales increased 2% at Free People and decreased 2% at Urban Outfitters and the Anthropologie Group, respectively. Wholesale segment net sales increased 40% partially due to delayed shipments from the third quarter carrying over into the fourth quarter. Co is now current on all Wholesale segment shipments and does not anticipate any further delays.

URBN reported EPS in-line on revs of $825.5 mln vs then- Capital IQ Consensus of $869.6 mln. The co had already fallen through support and sold off more than 20% in the week leading up to ER. The co initially gapped down 12% in extended hours trading, and it eventually ended the day down ~4% at $21.8. The Co has been on a tear in the last month, in conjunction w/ the rest of the teen retailers, and has regained the $28 level heading into earnings today.

Doesn't anticipate further sales misses due to delayed shipments

On March 3, Wunderlich reiterated its Hold rating. Wunderlich stated, "We have so far seen the teen segment face material pressure in 4Q from warmer weather, mediocre offerings, and a consumer still focused on bargains. Frankly, we believe Urban Outfitters has the potential to be impacted by all of these factors, with additional negatives from FX and weak tourist traffic. With somewhat weak initial Spring offerings, we see very limited upside and do not believe management will be optimistic in the near term; we remain on the sidelines. "

Its analyst price target is at $26.93 today, with a 52-week trading range of $19.26 to $47.25 and over the past 52 weeks the stock is actually down about 29%.

Comparable Retail segment net sales, which include comparable direct-to-consumer channel, decreased 2%. Comparable Retail segment net sales increased 2% at Free People and decreased 2% at the Anthropologie Group and 3% at Urban Outfitters. Wholesale segment net sales increased 29% partially due to delayed shipments from the third quarter carrying over into the fourth quarter.

This stock has had its roller coaster ride, to say the least. Initially, the stock opened at $47/share and doubled to about $90/share by May 22, but had a crash by mid-July, returning back to $40/share. Subsequently, it hit an all-time-low this past February, trading for as low as $31.88/share and since then has fallen nearly 11% from February’s last IPO price.

Currently, its March 11 share stands at $41.50. Also, note that its short interest is about 15% of its total float, but over the past few weeks has been decreasing recognizably. Its current volatility stands at 68%, which is 5% higher than its volatility over the past month, and the stock is expected to move its price 11% in either direction.

Same-store sales: increased 17.1% y/y

Shack sales (less revenue from licensing) in general increased 70% to $51.3 mln y/y

Updated FY15 Guidance (from Q3 earnings release)

Reaffirms total rev between $237-$242 mln vs $228.01 mln consensus

Same-store sales growth between 2.5%-3.0%

Key executives entered into share selling plans: CEO Randy Garutti, Chairman Daniel Meyer, & Director Jeff Flug. Garutti may sell up to 80,000 shares of common stock through Aug 31, 2016, which represent ~5% of his equity holdings. Meyer may sell up to 300,000 shares of common stock through Aug 31, 2016, representing ~5% of his equity holdings. Flug may sell up to 150,000 shares of common stock through Jan 2, 2017, which represent ~9% of his equity holdings in the co.

-Competitors Include: MCD, WEN, QSR, WING, DPZ, CMG, YUM

Same-Shack sales (LOL) increased 11.0% for Q4 vs. ests near +7%, on a calendar basis, versus 7.2% growth in the fourth quarter last year.

NMBL shares are down over 55% since it reported Q3 results when the company said there were two developments during that quarter that it believe impacted them. NMBL's investments in building out its large enterprise customer base is making progress, however these investments are taking to materialize. The second issue is the company shifted investments from commercial to large enterprise.

Las quarter the company reported Q3 Non-GAAP gross margin of 66.9% vs 67.1% in the same quarter as last year.

The company said it believes its planned investments will improve revenue growth as well as operating leverage over time. The company expects that it will take several quarters to realize the impact of these investments and have factored that into its guidance for Q4FY16.

Based on NMBL options, the current implied volatility stands at ~ 112%, which is 34% higher than historical volatility (over the past 30 days). Based on the NMBL March $10 straddle, the options market is currently pricing in a move of ~28% in either direction by weekly expiration (Friday).

NMBL shares have outperformed the S&P so far this year with NMBL gaining by 17% vs 5% loss in the index. NMBL tends to have 4-6% reactions to earnings. On a positive report, look for resistance near the $8.4, while support sits near $7.4.

**STATS FROM BRIEFING**

Shares of HTZ have been obliterated over the past 18 months. The stock is down 75% as increased competition from disruptive companies like $UBER have impacted pricing and margin while a hefty balance sheet and accounting issues have plagued investor sentiment. The industry remains under pressure as evident by the results posted by peer Avis ($CAR) on February 23.

Investors would like to see improving operating environment before finding an interest in this cast off name.

Net Income Margin- Q3 was 8% which was an increase of over 300 bps from the prior year.

Worldwide Car Rental Total RPD (RPD stands for Revenue per Transaction Day)- Q3 was $46.82, down 1% y/y. Investors would like to see sequential improvement here.

On 1/13 Reaffirmed initial 2016 outlook-

Separation of RAC and HERC on track for mid-2016.

On February 4 HTZ announced a private offering of $1.06 bln in medium term rental car asset backed notes. This fleet refinancing removed a major overhang on the stock as there was questions on whether or not rental car companies could even obtain financing. The co no longer has any corporate debt maturing in 2016.

Consensus calls for EPS of ($0.05) vs ($0.06) last year on revenue of $319.6 mln (+41% YoY)

Guidance for Q4 revenues of CNY 51.0-52.5 bln (+47-51% Y/Y)

GMV

During the Q3 conference call, JD stated that they suspect the macroeconomic headwinds in China may have some impact on their business. They also stated that they still see a very robust growth rate and that the overall consumption rate, at that time, had not been much impacted by the slowing macro environment.

Based on JD options, the current implied volatility stands at ~ 60%, which is 20% lower than historical volatility (over the past 30 days). Based on the JD Weekly Mar04 $26straddle, the options market is currently pricing in a move of ~11% in either direction by weekly expiration (Friday).

Stamps.com $STMP rallied 21% on Friday and was up as much as 25% at one point after reporting an astounding Q4 results and providing bullish guidance for 2016. This quarter exemplified the managements complete turnaround of the company and caught the analysts out of position (rare).

Stamps.com is a provider of Internet-based postage services and allows customers to buy and print postage on their computer without having to visit the post office. The company charges a monthly subscription fee plus postage cost. Its platform is also integrated in key partner programs like MS Office and $AMZN marketplace.

Historically the focus has been selling to individuals and small businesses. Recently however, the shift has gone towards more lucrative high volume shippers (warehouses, fulfillment houses/centers, boutiques and high volume retailers) and enterprise markets. This segment shift is more attractive on the margins side, ARPU, and lower churn rates. To get there, $STMP has been active on the M&A front. Its most prominent recent acquisition was buying Endicia from Newell Rubbermaid ($NWL). The deal closed in November 2015. Endicia is a major provider of high volume shipping technologies with seamless access to USPS.

In Q4 Non-GAAP EPS more than doubled YoY to $1.57, which was well above consensus of $0.95. Revenue rose 67.0% year/year to $69.9 mln, which also was well above consensus of $59.0 mln. $STMP also guided higher for 2016 as they expect non-GAAP EPS of $5.00-5.50 and revenue of $290-310 mln. Both were WELL above consensus with EPS being well above expectations: consensus was $4.33 and $289.7 mln, respectively.

Q4 Mailing and Shipping revenue was $67.2 million, up 67% YoY. In terms of margins, $STMP is highly profitable. Adjusted EBITDA margin for Q4 came in at 43.2% vs 30.5% in the prior year period. This margin expansion was huge and caught the street off guard.

$STMP says it was very pleased with its financial performance. Management says this was another exceptional year for Stamps.com with strong execution on its business goals. This included the integration of its 2014 acquisitions of ShipStation and ShipWorks where $STMP began to realize as it expected from those deals. In late 2015, STMP completed the Endicia acquisition and it has begun working on the process of integrating these businesses.

Record paid customers of 633,000 in Q4 was up 21% YoY and record ARPU, which was $35.35 was up 38% YoY. In addition, total postage printed for Q4 was $1 billion and that was up 71% YoY. For the year as a whole, total postage printed was $2.7 bln, up 52%.

On the call, management described how the business has transformed fairly dramatically over the past few years with a focus on growing its high volume shipping business and with its acquisitions of Endicia, ShipStation and ShipWorks. As a result of those acquisitions, $STMP now has a very wide range of customers and business models. Their shift from one off customers to larger volume shippers is the root of their turnaround.

This increased focus on shipping allows $STMP to expect revenue increases in seasonal periods. In particular, Q4 is expected to be meaningfully higher than the other three quarters due to the seasonally strong Q4 holiday shipping period as STMP saw in 2015. That said, don't expect the same in the 1st quarter of 2016.

$STMP adjusted EBITDA margins, which is a good proxy for cash flow, really sootd out. Q4 came in at 43.2% vs 30.5% in the prior year period. Those are some big margins. Expect that to moderate in Q1 and Q2 as these seasonally slower quarters will not benefit as much from spreading fixed costs over such a large revenue base. But even in the high 30% range is good.

Shares of SPLK have had a difficult start to 2016. SPLK opened up the new year trading at $59 but the stock is down nearly 40%. Valuation has been a key driver of the selling as the stock is trading at a very lofty 162x earnings. Even its sales valuation is frothy as it trades at 8x 2015 sales.

These high valuation, big data names were at the forefront when peer Tableau Software (DATA) reported results on February 4.

One thing that the co has done well in and that is quarterly performance. SPLK has steadily beaten on the top and bottom line and raised its outlook. In fact, Q3 saw an acceleration of revenue growth to 50% compared to 46% in Q2 and it marked its best top line growth in four quarters. The co will need to repeat this performance in order to help offset fears of an industry spend slow down.

SPLK Earnings Trading Activity

Key Metrics

Guidance

Q3 Recap

SPLK reported Q3 (Oct) earnings of $0.05 per share, excluding non-recurring items, $0.03 better than the Capital IQ Consensus of $0.02. Revenues rose 50.3% year/year to $174.4 mln vs the $160.31 mln Capital IQ Consensus.

Sprouts Farmers Markets (SFM) is scheduled to report 4Q15 earnings before the market opens tomorrow. The company reported last quarter's earnings at 8 AM ET (and a conference call is scheduled at 10 AM ET)

Guidance to Look For:

Last Q's Guidance for FY 15

Mid-Term Financial Targets

Other Guidance from Last Q

Analyst Commentary:

Peers: KR, WFM, TFM, WWAV