Current Quarter Expectations: As usual, operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Current Capital IQ consensus stands at Loss of $0.58 per share on Revenue of $194.3 mln.

Capital IQ consensus calls for Q3 adj. EPS of $0.37 on revs +3% to $3.72 bln.

Capital IQ Consensus calls for 2Q16 EPS of $1.39 & revenue growth of 18.9%, compared to 2Q15 EPS of $1.23 on revenue of $2.28 bln.

Twitter (TWTR) is set to report Q2 earnings tonight after the close with a conference call to follow at 5pm ET. Current Capital IQ consensus stands at EPS of $0.09 on Revenues of $607.4 mln.

Q3 Capital IQ consensus calls for EPS of $1.39 (versus $1.85 last year) on revenue of $42.126 bln (-27% YoY). The current consensus is near the mid-point of the company's guidance of $41-43 bln.

The current Capital IQ Consensus Estimates call for Q2 EPS of $0.94 and revenues of $3.09 bln. VZ expects full year 2016 adjusted earnings to be comparable to the co's full year 2015 adjusted earnings of $3.99 EPS

Freeport-McMoRan (FCX) is expected to report Q2 results tomorrow before the market opens with a conference call to follow at 10am ET.

Close to 40% of the S&P 500 will report their quarterly results this week. That includes McDonald's, which will report before the open on Tuesday.

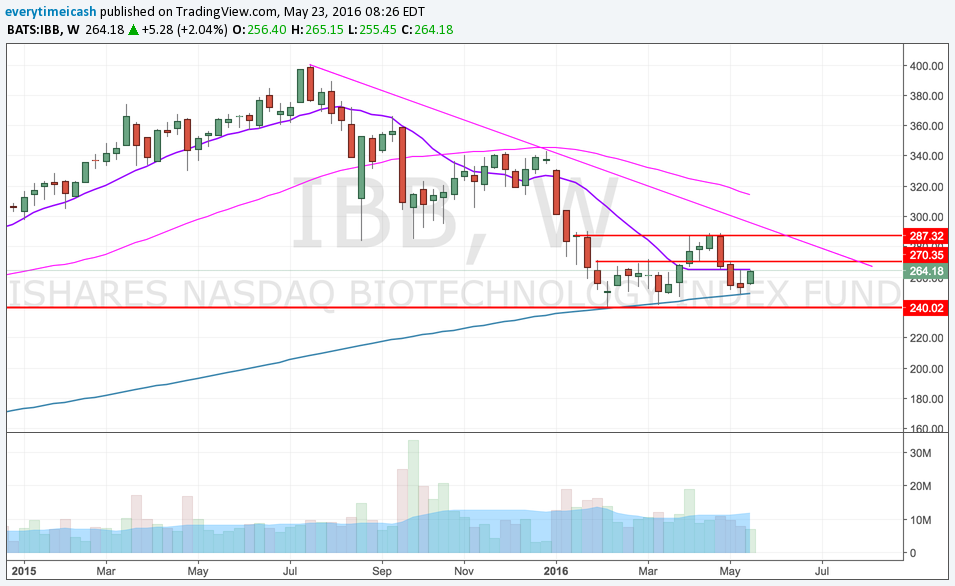

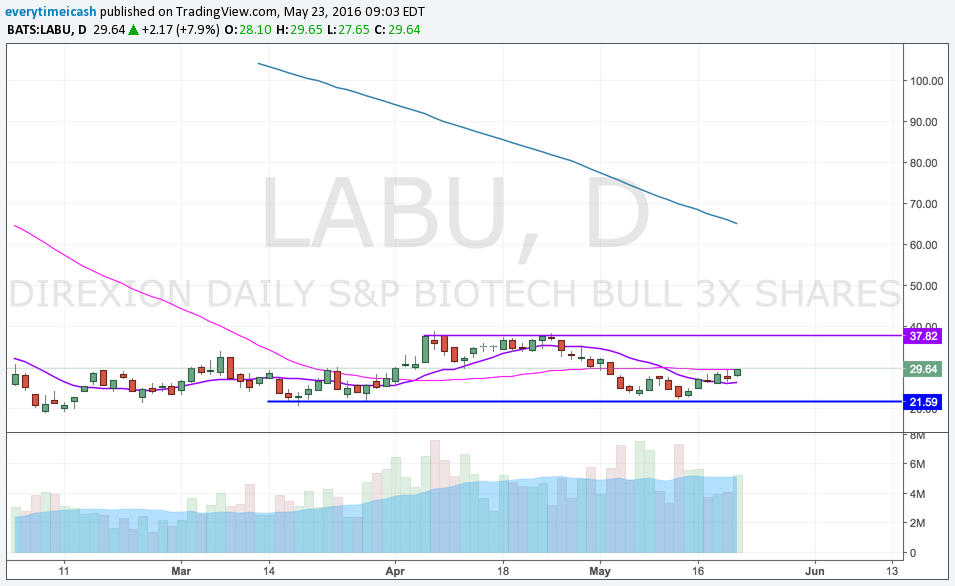

The question you ask yourself is: "How much can I risk with a 40% stop out and still fall under/at $100 loss on the day?"