There is little concern that FB will miss estimates this evening. FB is expected to provide an outlook for its Expense Guidance which is expected to come in well above the 2016 outlook of 40-45%.

Wolf's Den

Viewing entries in

Finance

There is little concern that FB will miss estimates this evening. FB is expected to provide an outlook for its Expense Guidance which is expected to come in well above the 2016 outlook of 40-45%.

No stock is as anticipated, nor will be scrutinized more closely, than the results from Apple, which will report after Tuesday's close

Oil and gas major-giant Exxon Mobil is scheduled to release its Q4 earnings results tomorrow Jan 31 pre-market with a conference call to follow at 9:30 am ET the same day.

Under Armour (UAA, UA) is set to report Q4 results tomorrow before the market opens with a conference call to follow at 8:30am ET. UAA is expected to report results at 7:15am. Last quarter the co provided its Q3 results at 7am and then provided prepared conference call remarks on its website shortly after the earnings release. Current Capital IQ consensus stands at EPS of $0.25 on revenues of $1.409 bln.

Guidance

Key Issues

Coach (COH) is set to report Q2 results tomorrow before the open with a conference call to follow at 8:30 AM ET. Co reported last quarter's results at 6:45 AM ET. Current Q2 Capital IQ consensus stands at EPS of $0.74 (vs. $0.68 last year) on revs up 2% to $1.32 bln.

WDC is expected to report second quarter earnings tonight after the close. There is a conference call scheduled for 17:00 (the company typically guides on the conference call).

IBM (IBM) will report Q4 results tonight after the bell with a conference call scheduled to start at 5:00 p.m. ET. Usually, IBM reports within the first 10 minutes after the bell.

NFLX had an aggressive International build in 2016. It also increased investment in its original content after so many of its shows (House of Cards, Orange is the New Black, Narcos, Stranger Things, etc) performed so well. The investments were complimented by a price increase that was 75% complete at the end of Q3.

Subs will remain topic of focus but investors want to see the company deliver. Especially with Forward P/E at a 145x 2017 earnings. The cash burn in Q3 was $506 mln and NFLX said it expected Q4 to come in at a similar level.

Domestic Streaming

International Streaming

NFLX SET TO TAKE OFF

Einhorn really put a damper on this stock yesterday as it confirmed an all time high breakout. It seems everyone from Carl Icahn to Einhorn want to take a shot at calling a top in this stock. "Valuation" is the obvious key concern for these guys, but it's all relative to how you value the stock. Take Amazon for example, it has been shot against on valuation for years now. That short selling and top calling has done nothing more than fuel Bezos' land buying spree.

NFLX has started to break out of a two year range and has cleared enough room for further upside. I want to play to capture that upside.

Excerpts from Shareholders Letter:

NFLX Key Metrics Courtesy of Briefing

Gigamon dives -18% on guidance; trading down near $38 after-hours. Next major area of support near June's breakout. This could be a foreshadow for darling stock NVDA IF they ever miss/soften their guidance.

The market will be paying close attention to several reports from the banking industry on Friday morning. The two "most important" being Bank of America and JP Morgan.

Shares of GOOGL hit an all time high of $838.50 on Monday but we have seen some profit taking ahead of tonight's report as the stock has pulled back to $820. The company is coming of an impressive Q2 in which it was able to accelerate revenue growth to over 20% for the first time in three years.

The growth was driven by Google website revenues as strength in the mobile and YouTube segments provided a boost. The rise in mobile has also boosted the growth in partners and website TAC which will be an area to watch.

The all time high will certainly be in play, especially when one views the Forward P/E of 20.5x being reasonable for a co that is posting 20%+ revenue increases despite being a $20+ bln a quarter company, no easy feat. A miss by GOOGL should prove interesting with the $783.50 Post-Q2 results being a key level of support. A break of this will send the shares to the $760 with the 200-sm ($757.29) in play.

Key Metrics

Q2 Recap

GOOGL reported Q2 (Jun) earnings of $8.42 per share, $0.38 better than the Capital IQ Consensus of $8.04. Revenues rose 21.3% year/year to $21.5 bln vs the $20.77 bln Capital IQ Consensus.

GOOGL/GOOG beats by $0.46, beats on revs

Current Quarter Expectations: As usual, operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Current Capital IQ consensus stands at EPS of $8.04 on Revenue of $20.77 bln.

Key Things to Watch

Twitter (TWTR) is set to report Q2 earnings tonight after the close with a conference call to follow at 5pm ET. Current Capital IQ consensus stands at EPS of $0.09 on Revenues of $607.4 mln.

Unlike many other companies, expectations for Facebook remain quite high. Failure to meet those expectations could cause a material decline in its stock, which is up 31% over the last 52 weeks.

Ad spending drives Facebook's top line, accounting for 95% of the company's revenue in 2015. FB is a barometer for how advertisers are spending and where they are allocating their advertising budgets.

Facebook has a large international presence with 86% of its 1.59 billion monthly active users at the end of 2015 residing outside the U.S. and Canada and 50% of its total 2015 revenue derived outside the U.S. and Canada. Facebook, then, will have some revealing insight to share on global economic activity and the impact of foreign currency on its operating results.

FB announced that the board of directors has approved a proposal to amend and restate existing certificate of incorporation to create a new class of non-voting capital stock, known as the Class C capital stock.

If approved, it will issue two shares of Class C capital stock as a one-time stock dividend in respect of each outstanding share of our Class A and Class B common stock. This proposal is designed to create a capital structure that will encourage Mr. Zuckerberg to remain in an active leadership role at Facebook.

“The adoption of the proposal is subject to the approval of our stockholders at our 2016 Annual Meeting of Stockholders to be held on June 20, 2016.”

FB breaks through all time high on stellar report, again.

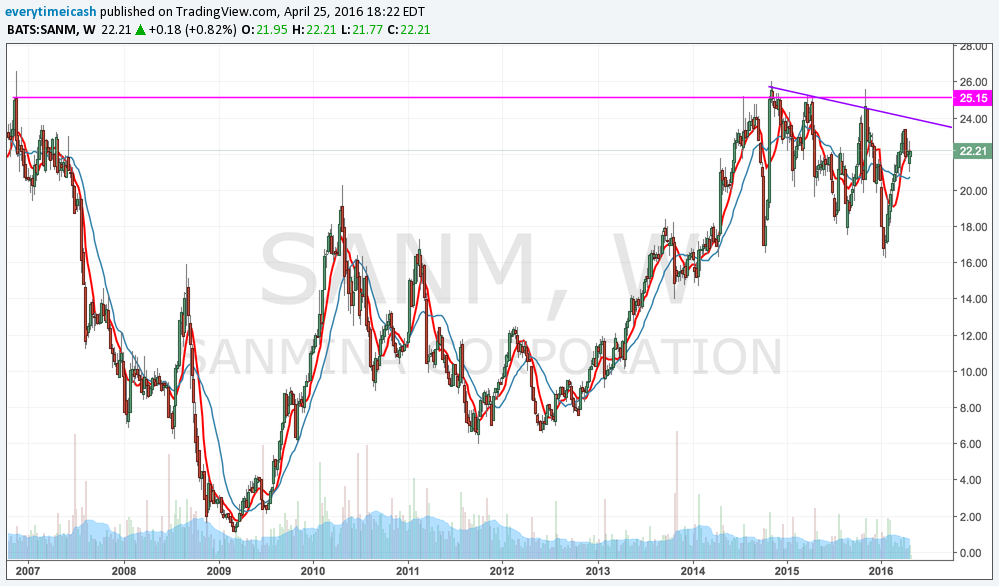

SANM is coming off a solid Q1 report. Its EPS were in line and its revenues actually missed expectations, but the revenue miss was expected. However, SANM operating margin was higher than expected and its Q2 guidance was also above consensus. The stock jumped 8% in reaction and has been a steady performer since as it would rally through a slew of key moving averages to push to $23.50.

Shares were ~30% higher from when it reported Q1 results. The stock has retraced back to its 50MA ahead of tonight's report. The decline is most likely some profit taking after a strong run during the quarter. The stock is sitting on its 50MA ($21.80) and has key support in the $21 zone.

Key Metrics

Q2 Guidance

Q1 Recap

SANM reported Q1 (Dec) earnings of $0.58 per share, excluding non-recurring items, in-line with the Consensus of $0.58. Revenues fell 9.9% year/year to $1.53 bln vs the $1.59 bln Capital IQ Consensus.

Capital IQ EPS consensus: 1.16 Capital IQ Rev consensus: 5.82 bln

Netflix ($NFLX) is set to report Q1 results tonight after the close with consensus at EPS of $0.03 on Revenue of $1.965 bln.

Q4 Recap: IBM beat on Q4 non-GAAP EPS of $4.84 vs the $4.81 Capital IQ Consensus and reported revenues in-line at $22.06 bln.